2016 was another volatile year for investors with the UK top 350 companies ranging from a low of 3,089 in February to a high of 3,931 in December, making a capital gain of 12.5% over the 12 months.

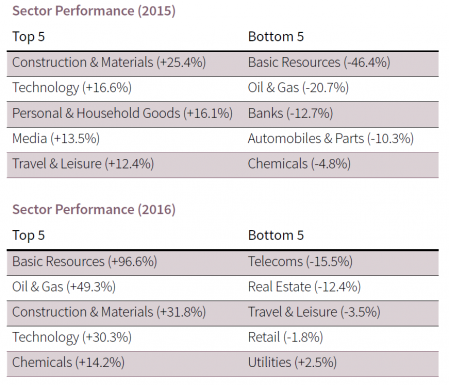

Looking in more detail, around 78% of all index returns, on a simple basis, were made from just two sectors, Basic Resources and Oil & Gas which showed gains of 97% and 49% respectively. If one were to include Banks, which made a gain of 8%, this figure would rise to a staggering 84%. Basic Resources benefited as copper and iron ore moved higher on hopes that growth in China is set to pick up again and that governments across the world will start to increase spending on infrastructure. Oil & Gas advanced following the Organization of the Petroleum Exporting Countries’ (OPEC) proposal to cut output. This pushed the oil price to the highest level in 18 months. Finally, Banks have been led higher by the international names, HSBC and Standard Chartered, gaining on the back of rising interest rate expectations and the potential for lighter regulation, following the success of Donald Trump in the US Presidential Election.

Basic Resources, Oil & Gas and Banks were in fact the three worst performing sectors of 2015, indicating that a contrarian approach would have paid dividends in 2016. These three sectors represented around 30% of the market at the start of 2016, rising to nearly 40% by the end of it, yet were responsible for the vast majority of the index’s return. This highlights the challenges faced by active managers: whilst passive trackers would have allocated funds in line with the underlying index weightings, meaning that performance would have been broadly in line with the index, not holding sufficient exposure to these sectors would most likely have led to significant underperformance. Sentiment has arguably changed on these sectors from extreme pessimism to the opposite extreme.

Whilst being heavily involved in these sectors in 2016 proved to be the right call, is outperformance likely again in 2017? It is a major concern that the strength in the Basic Resources sector is largely down to China which is dependent on ever increasing levels of debt to maintain its growth. With iron ore supply set to increase in 2017, the rally does not look sustainable. Even though the oil price has appreciated strongly from the lows, it is not perceived to be high enough to support the capital expenditure and dividend plans of the major oil groups. As a result, balance sheets in the sector are likely to continue to deteriorate. In response to OPEC, US shale producers are likely to react by increasing output, putting pressure on the oil price. Following a second increase in US interest rates in December 2016, it is questionable how much scope there is for any further increases, given the high levels of debt outstanding, not just in the US but globally. Any scaling back of expectations will be a major setback to the banking sector.

A contrarian approach suggests that now might be the time to consider other areas of the market. The worst performing sectors in 2016 were Telecoms, Real Estate and Travel & Leisure. Risks still remain in these areas, particularly with the uncertainty regarding Brexit, although they are arguably adequately reflected in current valuations. Food & Beverage and Health Care also underperformed in 2016 and also may present an opportunity for contrarian investors.

Whilst investors would clearly achieve the highest returns from investing in only the best performing sectors at the expense of all others, this focused approach would carry a much higher level of risk. However, it would appear sensible to tilt the portfolio towards areas which may have underperformed but look more attractive on a relative basis, whilst retaining an underweight position in other sectors. Fundamentals should not be overlooked and our preference would be for companies which have demonstrated consistency in earnings and free cash flow over the long term.

Source: Capital IQ