Retirement may seem a long way off for Millennials* but with people living longer and gold-plated final salary schemes disappearing from the pension landscape, the reality is that Millennials will need to work longer and save more than the Baby Boomers and Generation-X or face the prospect of a lower standard of living in retirement compared with previous generations.

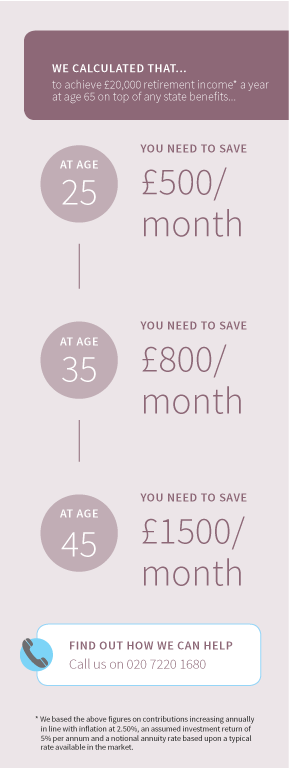

It would be very easy to say that the solution is to start paying into a pension as early as possible. We calculate that a 25 year old would need to save around £500 a month into a pension to achieve a retirement income of £20,000 a year when they reach age 65 on top of any state pension benefits to which you may be entitled. The cost goes up to more than £800 a month if they do not start saving until age 35 and increases to over £1,500 a month if it is left until age 45. At the time of writing, we have based these figures on an assumed investment return of 5% per annum and a notional annuity rate based upon a typical rate available in the market.

The introduction of auto-enrolment has helped and having an employer making pension contributions on your behalf means the option to join the workplace pension scheme is invariably a no-brainer; however this alone is unlikely to be anywhere near enough to provide a meaningful income in retirement. That said, making further contributions into a pension (in addition to those via a workplace pension scheme) that cannot be touched for more than 30 years may be unattractive and unaffordable if you are just starting out on your career, saddled with student debt, dreaming of owning your own home and wanting to start a family.

If you are looking to buy your own home then saving for a deposit may be a greater priority than saving into a pension for retirement. You may initially be better off directing your savings into a Help to Buy ISA or Lifetime ISA, into which you would receive a bonus from the government if the funds are put towards buying a home, although it is important to be aware that there are limits to how much you can contribute and potential penalties if funds are accessed for any purpose other than buying a home.

Another consideration is whether paying into a pension makes sense if you are a basic rate tax payer but see your career progressing and earnings increasing over time. As things stand, pension contributions attract tax relief at your highest marginal rate. This means for those who have just started out on their career and are earning £20,000 a year, then a pension contribution of £100 will cost you £80; whereas those earning £60,000 a year as a higher rate tax payer, that same £100 contribution will only cost them £60. In this scenario it may make sense to consider initially directing savings into an ISA and then paying this into a pension in the future at such a time when you can benefit from higher rate tax relief.

There is a definite need to make adequate provision for retirement and the greater the amount that can be saved the earlier on the better. However, this should not necessarily be restricted solely to paying into a pension as there is a need to consider priorities at different stages of life and plan accordingly.

Our expert financial planning team is available to help you or someone you know so please use our initial free consultation service to learn more about how we can help.

The above comments are of a general nature and are not intended to be construed as formal individual advice.

* The term Millennial is generally used to describe a person reaching young adulthood in the early 21st century.