Much was made last year of the post Brexit liquidity pressures placed on open ended property funds.

Following the shock result that the UK was to leave the European Union, there was concern amongst investors that the result could place pressure on the UK’s economic prospects and put off foreign investors as the pound sterling fell by the most in 20 years. This resulted in a higher than average number of investors asking to take their money out of open ended property funds. Fund managers found it difficult to cover the redemptions with cash. They were forced to sell property holdings and place their funds under a temporary dealing embargo or to penalise investors by lowering the values of their shares to account for the lower liquidity in the funds. The action taken gave managers time to raise cash funds to meet redemptions. This also had an impact on the Real Estate Investment Trusts (REITs) market, due to fears that confidence in property would be hit, as companies delayed decisions to expand their businesses with uncertainty over future growth. Post the event, open ended funds broadly adjusted their property portfolio valuations by between 5-15%, while share prices in REITs fell 15-30%.

REITs are a form of Close Ended Funds: Investors take a share in a pool of money. The original pool of investors have to sell their shares in the fund to exit.

Open ended Fund: In the opposite to this, the fund manager sells assets for investors to leave the fund, but can accept new investments into the fund at any time.

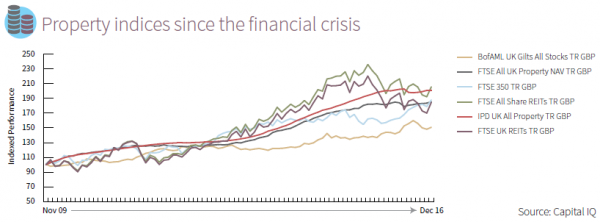

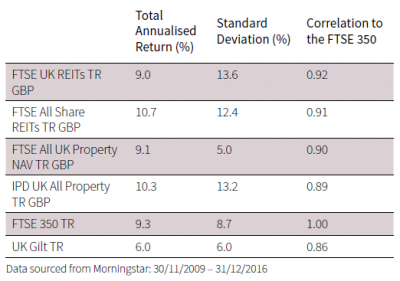

We have compiled a study on the performance of some of the UK’s major property indices on a total return basis against the Investment Property Database (IPD) valuation of UK property performance, the UK top 350 and UK all share gilts. Data is available for a seven year period. It concludes that over this time, property has outperformed the UK Gilts. In this case standard deviation represents the move away from the rolling average 12 monthly return and shows that although performance has been good, it has been more volatile than being invested in equities (UK top 350) or bonds (UK all share gilts).

Another interesting outcome is that the UK All Share REITs index has benefited from holding smaller property trusts who have exposure to niche developments, or sector specific growth such as healthcare; this greater diversification has also reduced volatility.

Conclusion

Property has been a strong performer over the period in question, benefiting from rising property prices, illustrated by the IPD indices. However, roughly two thirds of gains were derived from dividends received, this shows the importance of inflation linked income on returns. There was also a high correlation of performance against the UK top 350. Investors may be surprised that Property, which is seen as an alternative investment, will offer limited diversification to equities. Also, over the period there was considerably less volatility in the underlying net asset value (NAV- UK All Prop NAV TR) which may offer insight that diversion between the REITs’ share prices and the underlying NAV will revert in time. This highlights that although REITs may not suffer from the same liquidity risk as Open Ended Funds they will be susceptible to market forces, offering a different type of risk to investors. It is important to remember this is over a specific time frame and may not come to the same conclusion over a different period.