In our October issue, we discussed the concept of a benchmark. We observed that due to inherent biases, there is no such thing as a perfect benchmark.

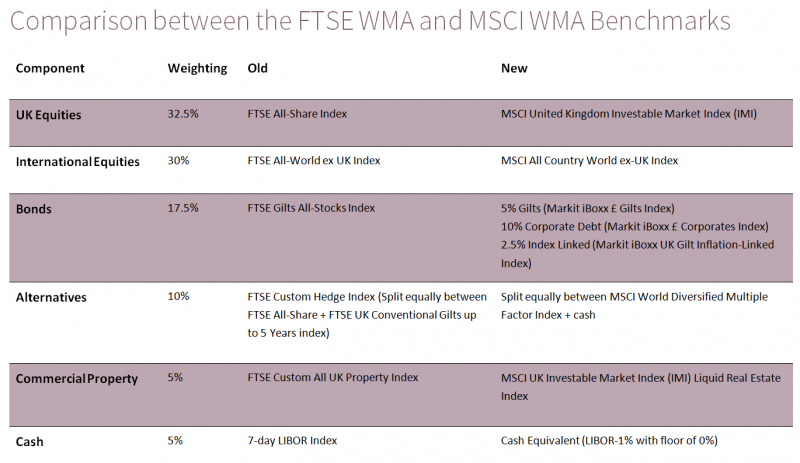

They can, however, present a useful starting point against which to measure performance. The Wealth Management Association (WMA) provides a range of benchmarks against which performance can be compared. As we indicated in October, the WMA would be switching its partnership from FTSE to MSCI. Its formal association with FTSE ended on 1 March 2017 and from this date, the benchmarks have been known as the MSCI WMA Private Investor Indices. Apart from the small print, what has changed? In line with the move to MSCI, there have been some subtle changes to the underlying components which make up the individual WMA benchmarks. We have summarised the changes below alongside the weighting of the components within the WMA Balanced Portfolio.

Explaining the Differences

Compared to the UK All-Share, the MSCI UK IMI is a more focused index because it does not invest in stocks with liquidity constraints. At the end of February, it had 352 constituents across large, mid and small cap segments of the UK market against 633 in the UK index. Looking at the international equities component, the MSCI index again has fewer constituents with only 2,375 against 2,941 in the UK market series, covering 85% of the global equity markets outside the UK. The bond exposure has been broadened out to include corporate debt and index linked gilts, reflecting feedback from member firms. Alternatives are now represented by a blend of cash and the MSCI Diversified Multiple Factor Index, an equity index which seeks to achieve returns through exposure to four factors: Value, Momentum, Quality and Low Size. Property has moved from an investable index of commercial properties to a liquid index which is based on the MSCI Core Real Estate Index, combined with short-term inflation protected bonds.

Given the changes to the benchmarks, what does this mean for investors? UK Equity will still be dominated by the same large stocks, which account for over 35% of the new MSCI index. With regard to the international equity, although the top ten constituents are identical in both indices, accounting for around 10% in total, the MSCI index has a higher weighting to the US but a lower position in Japan. The fixed income position will generate a higher level of equity risk from investing in corporate bonds and index linked securities. Alternatives will provide further equity exposure to the US which accounts for nearly 50% of the MSCI Diversified Multiple Factor Index, moving away from the UK exposure of the old index. In property, the new benchmark will provide an improvement in liquidity as it will move away from bricks and mortar investments to easily tradeable entities.

We do not believe it is necessary to change one’s investment strategy as a knee-jerk response. The WHIreland Asset Allocation Committee made a modest change to the fixed income exposure, introducing a small position in Index Linked Gilts, although this was more due to our current thinking on the immediate outlook for inflation than the benchmark change. In alternatives, our recommendation is to remain as diversified as possible with exposure to gold, total return and infrastructure funds to reduce volatility, increase income and overall risk-adjusted returns. The proposed alternatives component arguably does not fulfil the task of a true alternative investment by reducing overall portfolio risk by investing in assets uncorrelated with equities. By maintaining a constant position in equities and alternatives, one is likely to discover that the weighting relative to the US has in fact declined. Given stretched valuations in the US equity market at the current time, this may be no bad thing.

Overall we believe that the changes to the benchmark following the move to MSCI represent a step in the right direction. The underlying themes are of practicality and investability alongside a subtle shift towards increasing exposure to equities and US investments. As a benchmark, it is likely to be more representative of existing client portfolios.