There is no one-size-fits all solution to saving for school and university fees for your children’s future and while you may be aware that these fees are substantial, you may not have considered the actual cost or how to fund it.

The standard of education offered by independent schools and universities is valued by parents as you wish to give your children the best possible chance to achieve academically. Private school fees can be expensive and unfortunately, without forward planning, it is easy to significantly underestimate the real cost.

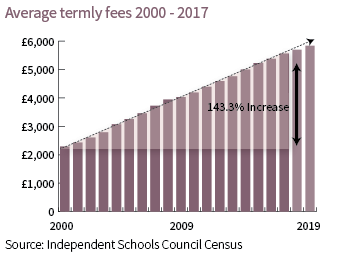

Fees for private schools are on the rise, in fact, fees have risen ‘four times faster than average earnings’ according to a study by Business Insider UK and they suggest that fees now represent 39% of the average salary of £34,500.

Assuming inflation of 2.5%, to put a child through 10 years of private education, as a day pupil, could cost £208,300. For a boarder, this figure could easily be doubled. If we consider the average increase in school fees over the past 17 years, this is actually an annual increase of 5.4% and the amount needed to fund school fees may well be more. What’s important to be aware of is that these figures are just the school fees and does not take into account the costs of the ancillaries such as uniform, school hobbies, trips and so on.

University fees, whilst not so imminent, also need to be considered. Fees increased this year to £9,250 per year and whilst your children can take out a student loan to cover these costs, the rates of interest are due to rise from 4.6% to 6.1% in the autumn. Your children are also entitled to maintenance loans to cover their living costs, e.g. food, books, accommodation and travel. Currently, this is £8,430 for those living away from home attending a university outside of London rising to £11,002 for those studying in London.

Up to 65% of this is non-means tested, whereas the balance is subject to the parental household income (the loan reduces where household income exceeds £25,000 as parents are expected to contribute to living costs).

As a drain on household expenditure, education costs will be significant, so what is a parent to do?

This all depends on what stage of life you are at and how much capital you have at disposal however, the 5 key things we believe you should consider are:

- Start planning early – How much can you afford to save per month?

- Make sure it will be affordable in the long term – If you do save, are you going to need to fall back on these funds in the event of a financial shortfall?

- Help from relatives – Are there grandparents that can and want to help and if so would they want to help with a regular contribution or with a capital lump sum? Grandparents are able to provide inter-generational assistance that also benefits their relatives as gifting money now may reduce their estate’s ultimate Inheritance Tax liability.

- Save tax efficiently – You can maximise your tax efficient savings through the use of your ISA allowances and also the Junior ISA allowances (the latter for university fees).

- Consider the level of investment risk you are prepared to take – Have you considered that the rate of interest on cash savings accounts will not keep up with the rate of inflation or rises in education fees and therefore erode the value of your savings?

Private school and university fees can be a significant concern however, with careful financial planning we can work with you to reduce the burden and stress of funding your children through their education. We achieve this by maximising the tax efficiency of your investments and target capital growth over and above that of school fees inflation.