World Market Summary

Equity markets recorded another very strong month in May, with the S&P 500 registering eight consecutive weeks of gains. The sky is no longer the limit for equity markets, with SpaceX looking to enter the public markets alongside Anthropic and OpenAI in the coming months. The three Initial Public Offerings (IPOs) are expected to fetch a valuation equal to that of the entire FTSE 100. The adage of ‘sell in May and go away’ has been less true over the last decade, but the increased issuance that comes with major IPO’s like these could put downside pressure on markets.

AI enthusiasm continues to be exceptionally strong, and importantly, remains grounded in the fundamentals, with the price movements supported by very strong earnings. This is best evidenced by the exceptional 13.7% Gross Domestic Product (GDP) growth displayed by technology-oriented Taiwan, which has translated into stock performance and resulted in Taiwan surpassing India to become the 5th largest stock market globally. Outside of Korea and Taiwan, which have benefited from the memory chip shortage, emerging markets (EM) have been more challenged in the face of US dollar strength.

This dollar strength has stemmed from the inflationary pressures that the Middle East conflict has given rise to. This has, in turn, led to an expectation that interest rates will remain elevated for longer, and hence bond yields rose globally in May. This was most stark at the long end of the yield curve, and particularly 30-year government bond yields. In the US, they surpassed 5% for the first time since 2007, in Japan, they surpassed 4% to hit all-time highs, and in the UK, they rose to 1998 levels. Although the new Chair of the Federal Reserve (Fed), Kevin Warsh, is outwardly in favour of lower interest rates, the current environment and the other members of the committee are expected to limit his capacity to do as he and President Trump would like.

Our in-depth views on:

Our weightings are based on sterling as a base currency.

United Kingdom (UK)

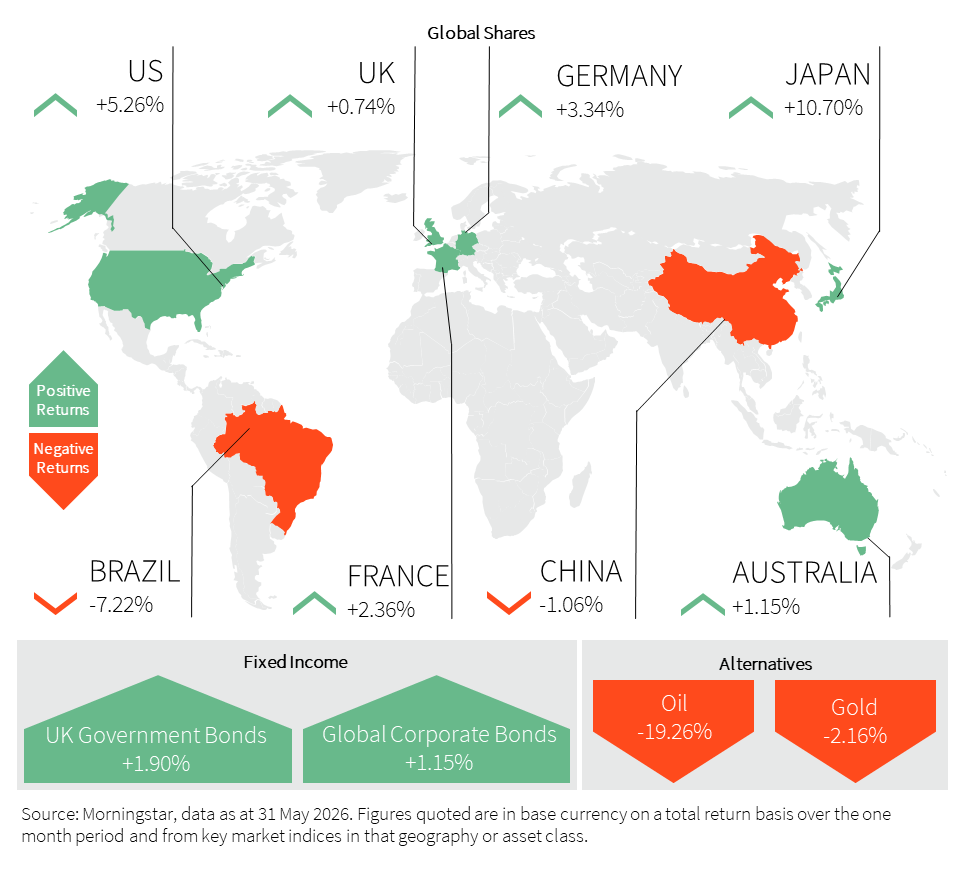

UK equity markets chopped around in May, ending the month in positive territory but underperforming many of the more technology-oriented global indices. It was a month that saw the FTSE 250 outperform, gaining 4.59%, in contrast to the FTSE 100’s meagre 0.74% return. This improved performance was driven by renewed takeover fervour as Tate and Lyle, Spire Healthcare, Bodycote and PPHE Hotels all received bids. In the case of Tate and Spire, the takeover premium to the prevailing share prices was over 50%, highlighting the disconnect that has existed between many mid-cap share prices and their intrinsic value. Should Tate and Lyle be gobbled up, it would be a historic final chapter for the FT 30, the original leading UK stock market founded in 1935, as Tate and Lyle is the sole surviving founding member.

Whilst progress on the Middle East conflict dominated international headlines, it was the fallout from Labour’s crushing local election defeats that lit up the domestic scene and in particular the UK gilt market. With over 70 MPs calling for Kier Starmer to step down, and Andy Burnham finding a place to stand, fears proliferated that Labour may lurch to the left and borrow more for public spending. The 30-year gilt yield hit the highest level for 28 years before easing back when Burnham confirmed he would stick to Labour’s self-imposed fiscal rules. He does, of course, have to win first in Makerfield in what is anticipated to be a hotly contested seat.

The UK economy expanded at a decent clip in the first quarter of 2026, gaining 0.6%, driven by health consumption and business investment. The data was, however, pre-Iran conflict, and the flash April Purchasing Managers Index (PMI) data showed a surprise contraction in the dominant services sector, displaying its weakest reading since January 2021. There was also weakness in the jobs market, with unemployment hitting 5% and the number of vacancies declining. Of real concern and highlighted by former minister Alan Milburn’s report is the scale of youth unemployment, which has the potential to lead to a ‘lost generation’.

There was better news on the inflation front as April’s reading came in at 2.8%, below the 3% expected, reducing immediate pressure for tighter monetary policy. Of particular note was the fall in core services inflation, which eased from 4.5% to 3.2%. Finally, weakness is showing up in the housing market with property prices falling by 0.6% in May, according to Nationwide, breaking a string of resilient spring gains as the effect of higher mortgage costs and falling consumer confidence hits. Whilst markets have been positive this year, housebuilding shares are in many cases down 25% to 50% year to date.

United States (US)

Those who sold in May and went away missed another roaring month for US equities. Nvidia anchored the AI trade, but it spread past the ‘Magnificent 7’ into hardware, semiconductors and mid-tier data centre stocks as the hyperscalers’ $750m capital expenditure* (CapEx) spend found new winners. The semiconductor index tracked by the Nasdaq has now gained 69% over the past two months.

Whilst on a price to earnings basis, the S&P 500 trades well above its historical average, the earnings growth witnessed in Q1 2026was exceptional and the strongest since 2021, which was flattered by a rebound from pandemic lows. Year on year, S&P 500 earnings grew by around 28%, with 84% beating estimates.

May marked a mixed month for US economic indicators, creating a continuing headache for the Federal Reserve when it comes to rate decisions in a climate of heightened macro uncertainty. The Fed’s preferred gauge, the Personal Consumption Expenditures (PCE) Index, rose in line with expectations at 3.8% over the year, with Consumer Price Index (CPI) coming in slightly hotter than expected in April, with energy inflation the main driver. GDP growth for the first quarter was revised down from 2.0% to 1.6%, with growth in consumer spending also being revised lower. Housing activity and consumer sentiment also weakened in the latest figures.

The labour market continues to demonstrate strong resilience at the moment. The unemployment rate held steady through spring at a rate of 4.3%, and the latest non-farm payrolls for April were well above consensus, adding 115,000 jobs against the 55,000-65,000 expected. This followed a similarly strong showing in March.

Europe

European equities rose over the month, with the Morgan Stanley Capital International (MSCI) Europe index up around 4.3%, but still underperforming global markets. Performance within Europe was uneven, with Italy leading gains, up 5.7%, reflecting relative strength in more cyclical and domestically driven parts of the market.

The macro backdrop remains dominated by inflation persistence and policy uncertainty. Eurozone inflation has re-accelerated, with inflation rising back towards 3%, driven primarily by a sharp rebound in energy prices. This has kept the European Central Bank (ECB) cautious, with recent minutes still indicating that some members see scope for further interest rate hikes, particularly if energy-driven inflation persists.

At the same time, growth remains subdued and uneven across the region. The Eurozone posted modest expansion in Q1 2026, with Italy outperforming on stronger domestic demand, while Germany and France continue to face weaker industrial activity and labour market softness. France’s unemployment rate has risen to 8.1%, and Germany is expected to see further deterioration from current levels. External demand has also weakened significantly, with exports to the US falling sharply following tariff-related disruption, leading to a marked decline in the Eurozone trade surplus. Economic sentiment is stabilising from very depressed levels, but remains negative, with indicators such as Germany’s ZEW, the Economic Sentiment Index, still in contractionary territory despite some improvement. Forward-looking signals suggest only a gradual and fragile recovery.

Overall, Europe continues to operate in a low-growth, inflation-sensitive environment, where energy shocks and geopolitical risks are increasingly driving the macro narrative. This sets a cautious backdrop with limited earnings momentum, divergent country performance, and ongoing uncertainty around the ECB’s policy path.

Asia and Emerging Markets (EM)

Emerging markets delivered positive but uneven returns in May, with gains driven by a narrow set of countries and sectors. Asia, excluding Japan, significantly outperformed, led by strong rallies in South Korea, up 22.2% and Taiwan, up 10%. In contrast, several large EMs declined, including Brazil which shed -7.2%, India -3.2%, and China -1.1%, underscoring the lack of breadth in the rally.

The dominant driver of returns was continued optimism around the AI CapEx cycle, which disproportionately benefited semiconductor-heavy markets such as South Korea and Taiwan. South Korean chip exports surged 151% in March, while Taiwan’s export orders rose 48.1% in April. Strong demand for advanced chips and electronic components continues to support earnings expectations and sustain momentum in the global AI supply chain.

Japan’s equity market reached new highs, with the Nikkei 225 up 10.7%, supported by better-than-expected economic growth and strong export demand linked to AI-related investment. Q1 2026 GDP grew at a 2.1% annualised pace, above expectations, driven by a rebound in private consumption and a robust contribution from net exports. Inflation continued to cool, with Tokyo core inflation easing to 1.3%, though still heavily influenced by government energy subsidies. Meanwhile, Japanese government bond yields rose sharply, reflecting structural forces including fiscal concerns and gradually normalising inflation expectations.

In China, sentiment remained mixed. While exports of electric vehicles, solar equipment, and AI-related inputs remained strong, domestic weakness persisted, with the housing downturn continuing to weigh on consumer confidence and spending. Retail sales were broadly flat, industrial production slowed to 4.1%, and property investment fell 13.7%. Regulatory pressure also resurfaced following a crackdown on offshore brokerages, weighing on Hong Kong equities.

Elsewhere, Brazilian equities were increasingly weighed down by rising food and fuel inflation, which is constraining the easing cycle, although a 0.25% interest rate cut at the mid-June meeting is still expected. The Bank of Mexico signalled a hold, without committing to a clear policy path.

Overall, May’s EM performance highlighted a market environment driven more by themes and factors than by country fundamentals, leaving returns increasingly sensitive to the durability of global AI investment.

Fixed Income

Bond market volatility picked up over the month, with yields moving sharply higher since the onset of the Middle East conflict. The US 10-year government bond yield has risen over 0.6% to 4.55%, while the 30-year yield has pushed above the key 5% level. The cause has been higher energy prices, adding to inflation pressures, prompting a meaningful repricing of the Federal Reserve outlook. Markets have moved from pricing two 0.25% cuts at the start of the year to now factoring in the potential for a rate hike, a dramatic shift that reflects the scale of uncertainty facing policymakers.

New Fed Chair Warsh was sworn in this month against a challenging backdrop. The April Federal Open Market Committee (FOMC) minutes showed officials growing more open to higher interest rates, with the majority flagging that further interest rate hikes would likely become appropriate should inflation continue running persistently above the 2% target, a level it has now exceeded for five consecutive years.

Elsewhere, UK and Japanese inflation both surprised to the downside, a welcome development for two central banks whose preferred stance remains wait-and-see as the Middle East conflict plays out.

The sharpest divergence of the month was between the US and Europe. US policymakers face building inflationary pressure compounded by a hot economy buoyed by AI CapEx spending. Europe, by contrast, is contending with the prospect of mild stagflation, where the energy shock simultaneously pushes up prices and weighs on growth, leaving conventional policy tools working against each other.

Alternatives

Oil markets showed tentative signs of relief in May, with Brent crude dipping towards $90 per barrel as rumours of a diplomatic breakthrough emerged. The US and Iran are reported to be negotiating a ceasefire extension of approximately two months, alongside discussions to reopen the Strait of Hormuz. The Strait has been closed since the conflict began on 28 February, putting a halt to around a fifth of global oil and Liquefied Natural Gas (LNG) supply. With the US midterm elections in November, the Trump administration has a clear political incentive to resolve the conflict and create conditions for the Fed to cut interest rates. However, even an optimistic resolution is unlikely to provide immediate relief with damaged facilities, disrupted supply routes, and record inventory depletion, meaning oil markets are expected to remain tight into 2027.

Gold prices edged down again over the course of May. The precious metal has struggled since the start of the conflict as the surge in bond yields has outweighed the increase in geopolitical uncertainty. As a non-yielding asset, the opportunity costs of holding gold increase as bond yields rise, and therefore it becomes a less attractive investment. After a very strong run, many have decided this is the opportune time to take profits. The more hawkish path for interest rates has been positive for the dollar, but once the conflict ends, interest rate expectations can once again be revised lower, and gold will once again look like the more attractive safe haven. However, one of the key trends that was helping gold move higher was central bank purchases, and worryingly, these have started to tail off, and this could prove to be a key challenge to the performance of the yellow metal going forward.

Property

UK housing momentum continued to ease over the month, with clear signs of slowing price growth and weaker buyer sentiment. Nationwide data showed annual house price growth cooling to 1.7% in May from 3.0% in April, alongside a 0.6% month-on-month decline, the first drop in five months. Royal Institution of Chartered Surveyors (RICS) survey data reinforced the softer tone, with the house price balance falling to -34%, its weakest reading since late 2023, indicating broad-based weakness in new buyer demand. Regionally, the market remains split, with London and the South of England under pressure, while parts of the North continue to show relative resilience. The main constraint remains affordability, with mortgage rates still elevated at around 6.6% and renewed energy-driven inflation risks weighing on expectations for interest rates. However, household balance sheets remain healthy, supported by low debt and sizeable savings buffers, which should help limit downside risk. Housing weakness could prove temporary if energy prices stabilise and geopolitical tensions ease.

In the US, the housing market is also showing clear sensitivity to higher rates. The 30-year mortgage rate has risen to around 6.7%, the highest in several months, driven by higher treasury yields amid persistent inflation concerns. This has translated directly into weaker demand in May, with mortgage applications falling over 8%, and refinancing activity dropping more than 18%, highlighting how rate-sensitive segments are being hit hardest. Purchase demand has also softened, though more moderately. Overall, both markets are being constrained by elevated interest rates and sticky inflation expectations, with housing activity increasingly dependent on the path of monetary policy. While there is no sign of a sharp downturn, the common theme across both the UK and the US is subdued activity, stretched affordability, and limited near-term momentum.

Learn more…

Capital expenditures (CapEx): CapEx is theinvestments that a company makes to grow or maintain its business operations.

For more industry terms and definitions, visit our glossary here.

Important Information

All Index data figures are sourced by Morningstar and correct as at 31 May 2026, unless otherwise stated.

The value of investments or any income arising from them may fluctuate and are not guaranteed. Past performance is not necessarily a guide to future performance.