World Market Summary

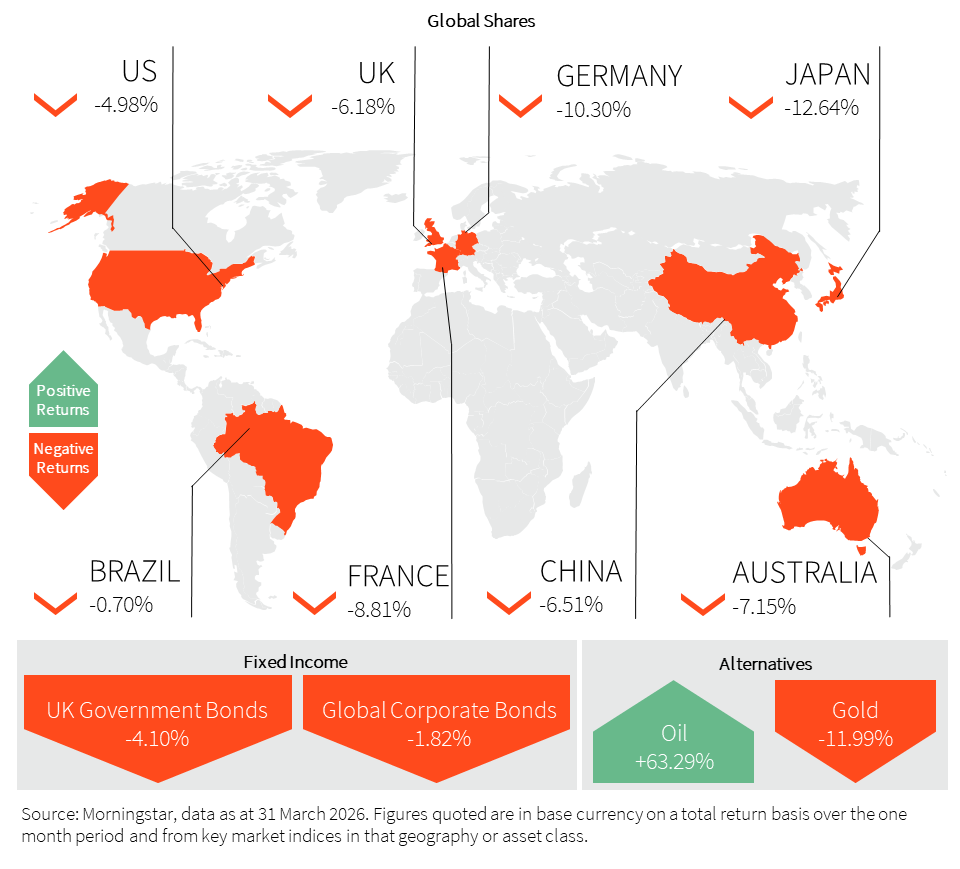

Market performance in March was naturally characterised by the events in the Middle East. Investors continued to be whipsawed by Trump’s constantly shifting rhetoric on the war, and unsurprisingly, by month-end, markets were a sea of red. However, given the severity of the situation and the record move in oil prices, the equity market reaction has been relatively contained, with the US market shedding just 4.98%. Granted, the US is better shielded as a net energy exporter, whilst economies which are more energy dependent, like Korea and Japan, have seen greater market sell-offs.

The effective closure of the Strait of Hormuz will continue to keep oil prices elevated, given that 20% of global oil and natural gas trade passes through the narrow waterway. This puts upward pressure on inflation, and therefore bond yields have risen as expectations for interest rate cuts have evaporated. The market is now pricing in a 40% chance of an interest rate hike in the US, as well as fully pricing three interest rate hikes in the UK and Europe. Global growth is also in jeopardy given the impact of higher energy prices on consumption, and this provokes a fear of stagflation. Ominously, the data is already feeding into this narrative with US Producer Price Inflation (PPI) reaching its highest in seven months, and the Atlanta GDP Fed Nowcast is tracking GDP growth at 2% for Q1, down from a figure of 4.3% in Q3 last year. The key determinant of the economic impact of the war will be its longevity. The ‘Liberation Day’ tariffs were quickly scaled back, and we have consequently seen five consecutive quarters of double-digit earnings growth from S&P 500 companies. Trump once again wants a quick resolution, given the upcoming mid-term elections, but this time, de-escalation is not simply reliant on the US President and could therefore take some time to reach a resolution.

There were also a few places to hide outside of equity markets, with government bonds and gold selling off. The precious metal had its worst month in over a decade, registering a double-digit loss as investors sought refuge in the dollar amidst the dramatic shift in monetary policy expectations. Whilst most central banks enter ‘wait and see’ mode, Brazil’s central bank decided to commence interest rate cuts from 2006 highs of 15%.

Our in-depth views on:

Our weightings are based on sterling as a base currency.

United Kingdom (UK)

The UK stock market experienced a volatile and challenging month in March. While the FTSE 100 traded near historic highs early in the period, it ultimately succumbed to global geopolitical pressures, ending the month down more than 6%, which was its 15th-worst monthly performance in 25 years.

The FTSE 100 initially continued to appreciate, fuelled by a record monthly public sector surplus and strength in commodity-linked stocks. However, as the Middle East conflict escalated, the index retreated sharply. This volatility was mirrored across the market, with small and medium-sized companies largely lagging behind their blue-chip counterparts.

The Bank of England (BoE) remained a focal point for investors. On March 19, the Monetary Policy Committee (MPC) voted unanimously to hold interest rates at 3.75%. While February inflation sat at 3%, the BoE warned that the spike in global oil prices and natural gas would likely delay the return to the 2% target, and inflation is now likely to stay trapped between 3-3.5% through the summer.

This market volatility and inflationary headwinds also caused a raft of major institutions to slash their 2026 growth forecasts. GDP growth projections were cut from 1.1% to as low as 0.5% by firms such as Oxford Economics and Barclays.

The Housebuilding sector was the month’s biggest detractor. Persimmon fell some 29% despite seemingly robust annual results, while Barratt Redrow declined over 28% due to fears that sticky inflation would force interest rates higher for longer.

Within commodities and energy, Shell and BP saw heavy trading volume as oil prices surged, and as such, they managed to buck the trend, seeing their share prices rise over the month. On a more esoteric footing, Raspberry Pi managed to appreciate more than 15%, albeit not without volatility, as investors found a rare bright spot in high-growth and more niche technology.

United States (US)

The US stock market endured a gruelling first quarter, with March marked by significant volatility and a heavy risk-off sentiment. While the month began with a steep sell-off that erased all year-to-date gains, an end-of-month rally sparked by hopes of a diplomatic resolution in the Middle East helped indices recover some lost ground, though they remained deeply in the red for the quarter.

The major indices saw their worst quarterly start in years. By the close of March, the Nasdaq 100 and S&P 500 had both shed nearly 5% for the month, while the Dow Jones Industrial Average fell 5.2%. Indeed, early in the month, the S&P 500 tested its 200-day moving average as futures collapsed amid surging oil prices.

The Federal Reserve (Fed) remained the centre of gravity for macro sentiment. At its March 18 meeting, the committee voted to hold interest rates steady at 3.5–3.75%. While headline Consumer Price Inflation (CPI) showed signs of stabilising earlier in the year, the Fed raised its expectation for its favoured measure of inflation, Personal Consumption Expenditure (PCE), to 2.7%, given the ‘uncertainty’ from the Middle Eastern conflict and soaring energy costs. Despite the hawkish hold, the Fed’s forecast still suggested a 0.25% interest rate cut remains likely before the end of the year, providing a small glimmer of hope for a late-year pivot.

March was a somewhat historic month for consolidations despite the backdrop. Most notably, McCormick, which reached a $44.8 billion agreement to combine with Unilever’s global foods business right at the end of the month.

On a sector level, traditional energy stocks and defence contractors saw heavy inflows, contrasting sharply with the ‘Magnificent Seven’ technology giants, which struggled under the weight of rising yields despite the world’s largest company, Nvidia, projecting $1 trillion in sales through 2027.

Digital asset companies like TenX Protocols gained attention as institutional interest in blockchain infrastructure remained resilient despite the broader equity downturn.

Europe

MSCI Europe ex-UK Index declined 8.2% over the month, with Germany the largest laggard, down 10.3%. Even before the escalation in the Middle East, the disinflation trend was coming to an end. Eurozone CPI rose to 1.9% in February from 1.7% in January, exceeding market expectations. Against this backdrop, the European Central Bank (ECB) kept interest rates on hold and raised its 2026 inflation forecast to 2.6%. President Christine Lagarde highlighted that higher energy prices are likely to have a material impact on near-term inflation, reinforcing a cautious policy stance.

The macro impact is increasingly evident across activity indicators, particularly in energy-sensitive economies. Eurozone consumer confidence fell sharply below its long-term average to mark the largest decline since March 2022. Industrial production also weakened, recording its largest monthly decline since April last year, driven by contractions in non-durable and capital goods.

As highlighted by performance, Germany’s economy has been disproportionately affected. Factory orders fell 11.1% month-on-month in January, significantly worse than expected, with domestic demand down 16.2% and exports also declining. The data point to a broad-based slowdown, reflecting both weaker external demand and rising cost pressures.

Prolonged energy price pressures are likely to weigh further on consumer sentiment and industrial activity, suggesting downside risks to near-term growth.

Asia & Emerging Markets

Emerging markets significantly underperformed amid the global risk-off environment, with the FTSE Emerging Index falling 10.3%, nearly double the decline of the FTSE World Index. Performance dispersion was largely driven by energy exposure and vulnerability to supply disruptions.

China proved relatively resilient, with the SSE Composite Index down 6.5%, supported by its diversified energy mix and constructive ties with Iran. While roughly half of China’s oil imports transit through the Strait of Hormuz, oil accounts for less than 20% of its primary energy consumption, limiting the immediate impact. Policymakers also intervened to cap domestic fuel price increases. February macro data surprised to the upside, particularly in exports, industrial production and fixed asset investment. However, underlying weakness persists, with falling home prices continuing to weigh on consumer confidence.

By contrast, Japan was one of the hardest hit, with the Nikkei declining 12.6%, reflecting its heavy reliance on imported energy. Around 95% of Japan’s oil imports come from the Middle East, with a significant portion passing through the Strait of Hormuz, raising concerns over higher input costs and pressure on growth. Inflation data pre-dating the conflict were softer than expected, but spring wage negotiations delivered over 5% increases for a third consecutive year, pointing to persistent inflationary pressures.

Elsewhere in Asia, South Korea announced a bond buyback programme to stabilise markets amid rising yields and tighter financial conditions. India took a more targeted approach, cutting fuel taxes to limit the impact on consumption, albeit with longer-term fiscal implications.

In Latin America, Brazil and Mexico were comparatively resilient given their oil export exposure. While inflation surprised to the upside ahead of the oil shock, Mexico cut interest rates by 0.25 percentage points against expectations of a pause, while Brazil delivered a smaller-than-expected 0.25 percentage point interest cut, marking the start of its cutting cycle.

Fixed Income

Interest rate markets repriced sharply as risks of sustained higher inflation increased, with interest rate expectations in the Eurozone, UK and US moving materially higher. Major central banks, including the Fed, ECB, BoE and Bank of Japan (BoJ), kept interest rates on hold but adopted a more hawkish tone in response to rising energy prices.

The repricing was most pronounced in the UK. Two-year gilt yields rose by around 0.9 percentage points, while 10-year yields increased by approximately 0.6 percentage points. Markets have shifted to price roughly 0.85 percentage points of additional interest rate hikes by year-end. Even prior to the escalation in the Middle East, inflation remained sticky, with February services inflation at 4.3% and core inflation at 3.2%. With higher energy prices feeding through, headline CPI is now expected to move back towards 4%.

In the US, the Fed held interest rates steady as expected, but market pricing shifted meaningfully, with expectations moving from two interest rate cuts to no cuts in 2026. Similarly, the ECB kept policy unchanged, while markets now price around 0.75 percentage points of further interest rate hikes. Updated forecasts reflected higher inflation and weaker growth, highlighting stagflationary risks. In Japan, the BoJ also held interest rates but signalled openness to further monetary policy tightening, with markets pricing around 0.46 percentage points of hikes by year-end.

Alternatives

Brent oil prices surged dramatically in March, rising by 63%, the largest monthly increase since 1988. By the end of the month, Brent crude for May delivery reached around $118 per barrel, while US oil also saw a strong monthly gain of 51%, despite some price declines toward the end of the period.

While the US appears to be considering de-escalation, Iran still has incentives to maintain pressure, making the conflict unpredictable. Trump has also issued strong warnings, threatening to target Iran’s energy and infrastructure if the Strait is not reopened. Iran’s attack on a Kuwaiti oil tanker near Dubai towards the end of the month demonstrates its continued ability to disrupt key shipping routes and tighten control over the Strait of Hormuz.

Oil shipments through the Strait of Hormuz, normally responsible for about 20% of global oil trade have nearly stopped since the conflict began. Analysts warn that further escalation, including potential US ground operations, could prolong the war and increase both economic and human costs.

Gold saw a modest rebound at the end of March, but still recorded its steepest monthly decline since October 2008, falling around 11.8% overall. This was driven by rising inflation concerns and the resulting expectations of higher interest rates. Higher interest rates reduce the appeal of gold because it is a non-yielding asset, thus increasing the opportunity cost for investors.

A stronger US dollar, which also gained over the month, made gold more expensive for international buyers, adding further pressure on prices.

Property

The UK housing market picked up pace in March, with prices rising 2.2% compared to a year earlier, up from just 1.0% in February and the fastest growth since last October. The average house price hit a record £301,151 with monthly prices increasing by 0.3%, adding to earlier gains, and lifting the average house price by £3,000 since the start of the year. This suggests housing demand is improving, but the Middle East conflict is likely to weaken demand going forward as rising inflation expectations put upward pressure on mortgage rates.

Despite this, the overall picture remains relatively stable, supported by a strong job market, low household debt, healthy savings, and the fact that 90% of mortgages are on fixed rates.

Meanwhile, the construction sector is struggling. The UK Construction Purchasing Managers Index dropped more sharply than expected in February. Companies reported fewer new orders, weak demand, and disruptions from poor weather. Housebuilding was hit the hardest, followed by declines in infrastructure and commercial construction. However, there is some optimism, with business confidence reaching its highest level since late 2024, as firms expect more contracts and better economic conditions ahead.

Learn more…

For more industry terms and definitions, visit our glossary here.

Important Information

All Index data figures are sourced by Morningstar and correct as at 31 March 2026, unless otherwise stated.

The value of investments or any income arising from them may fluctuate and are not guaranteed. Past performance is not necessarily a guide to future performance.