World Market Summary

As the World Cup commenced, markets paused for hydration in what was a very strong half (year) of performance. Both the South Korean national team and market participants will want to forget June’s performance, but memory remains key to the longevity of their market rally. Memory chip-maker Micron is also playing a key role in US market performance as its stellar earnings boosted the stock, but subsequent price hikes from the likes of Apple and Microsoft incited fears that Micron’s customers are struggling to cope with elevated memory prices.

The record Initial Public Offering (IPO) from SpaceX pushed Elon Musk to dollar trillionaire status, initially gained a lot of traction with investors before the stock fell back along with broader US tech sentiment. Thus far, the old adage of ‘sell in May and go away’ has proved a good strategy. Still, earnings remain strong and grounded in fundamentals, which enables us to remain optimistic for equity performance prospects in the coming months.

The Memorandum of Understanding between Iran and the US helped oil prices to subside, but markets instead focused on commentary from the new Federal Reserve (Fed) chair, Kevin Warsh. He hinted at the prospect of interest rate hikes, which added to downside pressures on equities, and the reassurance he provided on the Fed’s independence added to downside pressure on gold. The precious metal dropped below $4,000 for the first time since November. Warsh’s commentary also limited the reaction from US Treasuries to the drop off in the oil price. Meanwhile, in the UK, gilts were free to rally in response to the oil move as bond markets largely looked through the resignation of Keir Starmer.

Turning to economic data, US core Personal Consumption Expenditure (PCE) hit the highest level since 2023 at 3.4%, which is well in excess of the Fed’s 2% target. Consumer confidence picked up from record lows as oil prices fell. Economic growth and the labour market have shown signs of stabilisation, but given the fall in oil prices and wage growth remaining in a disinflationary trend, the Fed will likely remain on hold over the coming months. Elsewhere, the Bank of England (BoE) also held rates constant, but appears to have a greater capacity to cut interest rates in the coming months. Meanwhile, the European Central Bank (ECB) ended its interest rate-cutting cycle, opting for a hike in response to the pick-up in inflation. The Bank of Japan (BoJ) also hiked as wage growth looks increasingly embedded in the economy. Finally, Brazil continued with interest rate cuts.

Our in-depth views on:

Our weightings are based on sterling as a base currency.

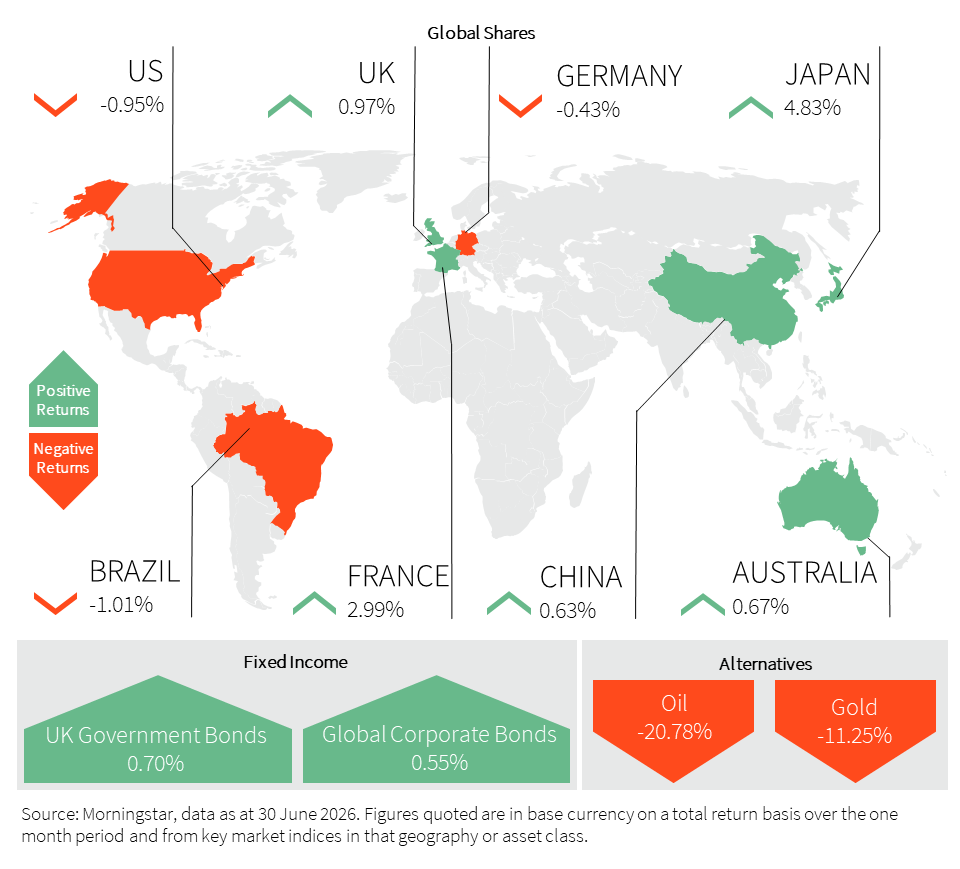

United Kingdom (UK)

UK equities delivered mixed performance in June, with a clear divergence between internationally exposed large caps and domestically sensitive mid-caps. The FTSE 100 posted a modest gain, supported by its defensive sector composition and global earnings exposure, while the FTSE 250 fell 1.5% amid political uncertainty and continued weakness in domestic activity.

Political developments were a key driver of sentiment. Prime Minister Keir Starmer resigned following sustained pressure, triggering a leadership transition. Andy Burnham is widely expected to succeed him, while attention has also turned to the likely appointment of Ed Miliband as Chancellor. The Burnham–Miliband pairing is viewed by market participants as fiscally expansionary, but it would operate within a highly constrained fiscal backdrop, limiting near-term policy flexibility and contributing to uncertainty in domestically-oriented equities.

The BoE held policy rates unchanged, in line with expectations. The Monetary Policy Committee (MPC) noted that recent energy price increases are likely to push the Consumer Price Index (CPI) towards a peak of around 3.25% in Q4 2026, but they reiterated confidence that the broader disinflation process remains intact. Lower-than-expected inflation data in April and May this year, combined with weak activity data, reduced the urgency for further interest rate hikes.

Economic data remained subdued. Retail sales fell sharply in June, reflecting weak consumer confidence and persistent cost pressures, reinforcing concerns that domestic demand remains fragile despite some improvement in real income dynamics.

Overall, June highlighted a continued divergence between globally exposed UK equities and domestically driven sectors, with political uncertainty and weak activity continuing to weigh on sentiment.

United States (US)

After the blistering run in April and May, the S&P 500 and Nasdaq paused for breath in June as valuation concerns in the major Artificial Intelligence (AI) stocks led to some rotation away from this sector. That said, the Nasdaq still managed to notch its best quarterly performance in six years. As is usually the case when the Nasdaq weakens, we see an outperformance in the Dow Jones Index (DOW), which rose 2.71% through the month and ended the period around its record high.

The month was also marked by the flotation of SpaceX, Elon Musk’s rocket and satellite business. The company achieved a valuation in excess of $2trillion despite reporting a near $5bn loss in 2025. The successful IPO led to Elon’s wealth surging, and he became the first dollar trillionaire. This marks the start of a number of high-profile trillion-plus flotations which include Anthropic and OpenAI.

June marked Warsh’s first month as the new Fed chair, and as expected, interest rates were kept in the target range of 3.5% to 3.75%. There was, however, a more hawkish tone to their messaging and they significantly raised their inflation forecasts. Further comments from Warsh at the ECB Forum on Central Banking outlined his priority to get inflation back to 2%.

Headline CPI rose 4.2% year on year in May, which was the highest reading since April 2023. This was largely due to the significant rise in energy prices. On a more positive note, core CPI for the month moderated. The Fed’s preferred gauge, the PCE Index, reflected a similar pattern to CPI. Despite higher inflation, consumer confidence improved, and retail sales surpassed expectations, underlining the resilience of the US consumer.

Europe

European equities outperformed global markets in June, supported by improved risk sentiment. Gains were led by France, Italy, and Spain, where easing energy concerns and stronger confidence supported performance, while German equities lagged, with the Deutscher Akitenindex (DAX) ending the month lower due to higher sensitivity to global trade and energy-related uncertainty.

The improvement in geopolitical risk fed directly into sentiment indicators. Germany’s ZEW Indicator of Economic Sentiment recorded its largest monthly increase since 2022, turning positive for the first time since the start of the Middle East conflict. Activity data also showed tentative stabilisation, with Purchasing Managers Index (PMI) rising to the highest level since March and above expectations, although still marginally below the expansion threshold. Manufacturing remained in expansionary territory for a fifth consecutive month, albeit with some moderation.

Inflation continued to ease. Eurozone CPI fell to 2.8% in June from 3.2% in May, below expectations and the lowest reading since before the energy shock linked to the Middle East conflict. Inflation expectations also declined, reinforcing signs of moderating price pressures.

Against this backdrop, the ECB raised rates by 0.25%, but subsequently shifted towards a more patient stance. Policymakers highlighted slowing growth and improving inflation dynamics, while falling oil prices reduced expectations of further tightening. This also weighed on the euro following softer German inflation data.

Asia and Emerging Markets (EM)

Emerging Markets (EM) underperformed over the month, with US dollar strength and rising US interest rate expectations acting as a broad headwind to risk appetite and asset performance.

Japan was the strongest performer, with the Nikkei up 4.8%, supported by falling oil prices, which eased imported inflation pressures and improved terms of trade. The BoJ raised interest rates to 1%, in line with expectations, while signalling a slower pace of quantitative tightening from 2027. Policy commentary edged marginally more hawkish, with board member Naoki Tamura advocating a faster move towards neutral rates, estimated to be around 2%. At the same time, Prime Minister Sanae Takaichi announced a large-scale fiscal investment programme of around ¥370 trillion (USD 2.3 trillion) through 2040, reinforcing longer-term growth support.

China data disappointed on balance, with domestic weakness offset only partially by external resilience. Retail sales contracted for the first time since 1990, excluding the COVID period, underscoring weak consumption momentum. Industrial production proved more resilient, supported by export demand, while trade data again exceeded expectations but was largely price-driven, particularly in semiconductors and energy. Producer price inflation rose to its highest level since 2022, reflecting upstream cost pressures rather than demand recovery. Property remained the key drag, with investment down 16.2% and continued broad-based declines in home prices.

Elsewhere in EM Asia, AI-related investment remained a key structural support. In South Korea, Samsung and SK Hynix announced a combined $518 billion investment programme in memory capacity, reinforcing the durability of the AI capital expenditure (CapEx) cycle. In India, Amazon committed a further $13 billion to expand AI and cloud infrastructure, sustaining digital investment momentum.

Latin America was mixed. In Brazil, the central bank cut the interest rate by 0.25% to 14.25%, marking a third consecutive reduction, but the central bank adopted a more cautious tone as both growth and inflation re-accelerated, with policymakers warning that fiscal stimulus could further complicate the inflation outlook. In Mexico, the central bank unanimously held interest rates unchanged, with the easing cycle effectively declared over in May, while this year’s GDP growth forecast was raised from 1.6% to 2%, supported by stronger Q1 2026 activity, agriculture, and credit and fiscal stimulus.

Fixed Income

Bond market volatility remained relatively subdued in June, but after elevated inflation data in the US and the Fed’s hawkish commentary, the market moved to price in at least one interest rate hike this year. Nine of the 18 policymakers at the Fed are expecting at least one hike this year, and six are expecting more than one. However, Warsh has been keen to limit forward guidance, he has talked of AI productivity gains putting downward pressure on inflation, and the recent decline in oil prices will also work to this effect. Therefore, we are still sceptical that the Fed will move to hike interest rates in the coming months. If this holds true, treasuries will rally as the bond market adjusts to our view.

Whilst treasuries remained largely unmoved in June, UK gilts rallied as they shrugged off Keir Starmer’s resignation and turned more optimistic on the Bank of England’s capacity to cut interest rates in the coming months.

Despite the BoJ’s decision to hike interest rates, the yen remains at an all-time low, having surpassed ¥160 against the dollar. The BoJ will likely step in again to defend the currency, having spent ¥11.7 trillion last year to prevent it from going higher than ¥160 against the dollar.

Finally, credit spreads tightened after the short-term widening associated with the Middle East conflict.

Alternatives

Gold dropped below $4,000 for the first time since November, before recovering slightly above this key technical level in time for the month-end. However, it has still registered four consecutive monthly declines amid Middle East uncertainties and expectations that the Fed will raise interest rates this year. Markets continue to price in at least one rate hike by the Fed this year, with the first potentially coming as soon as September 2026, while some investors are betting on additional hikes thereafter. The precious metal has declined about 11% this month and close to 14% this quarter. Investors are now awaiting the latest US monthly employment report for fresh clues on the policy outlook. Meanwhile, the US and Iran are scheduled to resume peace talks in Qatar, although prospects for a lasting ceasefire remain unclear. A major sticking point remains after Tehran reiterated its plan to oversee traffic through the Strait of Hormuz even if Oman decides not to take part.

Copper prices fell below $6.10 per pound as investors awaited a US Commerce Department report that could lead to tariffs on refined copper imports. Strong US economic data also weighed on prices by increasing expectations of a tighter Fed policy, raising concerns over industrial metals demand. Despite the short-term weakness, Goldman Sachs remains constructive on copper’s long-term outlook, citing growing demand from electric vehicles, renewable energy, defence spending and AI infrastructure.

Brent crude oil ended the month just above $70 per barrel, recording a near 30% drop in Q2 2026, which represents its largest quarterly decline since 2020. This plunge follows a surge in supply as traffic accelerated through the Strait of Hormuz after progress toward a peace deal released oil previously trapped inside the Persian Gulf. Additionally, US sanction waivers granted to Iran have introduced extra volumes into a market already trying to absorb major supply workarounds.

Property

The Halifax House Price Index (HPI) showed UK house prices rose 0.5% in May on an annual basis, which was below the expected 1.0% increase and following a 0.4% gain in April. On a monthly basis, prices fell 0.1%, matching the decline recorded in April and contrasting with forecasts of a 0.1% increase. Amanda Bryden, Head of Mortgages at Halifax, noted that uncertainty surrounding developments in the Middle East and higher inflation expectations have kept borrowing costs elevated, weighing on affordability and consequently demand. Still, housing market activity has remained resilient, with transaction levels holding relatively steady.

The RICS UK Residential Market Survey showed that the house price balance remained at the weakest level in November 2023.

Construction PMI signalled the sharpest contraction in construction activity since May 2020. Housing remained the weakest-performing segment, while commercial and civil engineering also declined amid client caution linked to inflation and geopolitical tensions. New orders fell at the fastest pace in six years as project delays, deferred investment decisions, and budget cuts weighed on demand. Consequently, employment and purchasing activity continued to decline. On the price front, input cost inflation accelerated to its highest level since June 2022, driven by higher fuel and transport costs.

Important Information

All Index data figures are sourced by Morningstar and correct as at 30 June 2026, unless otherwise stated.

The value of investments or any income arising from them may fluctuate and are not guaranteed. Past performance is not necessarily a guide to future performance.