World Market Summary

February saw a substantial spike in equity market volatility as AI, tariff and geopolitical uncertainty mounted. Valentine’s Day didn’t prove contagious, as the four-year anniversary of the start of the Ukraine-Russia war came and went with peace still no closer. We also saw an escalation in the Middle East as US-Iran tensions picked up. Meanwhile, the release of Anthropic’s latest AI model caused a major sell-off in software stocks, holding a Claude over US markets and provoking further broadening out of performance away from US stocks despite strong earnings from the world’s largest company, Nvidia.

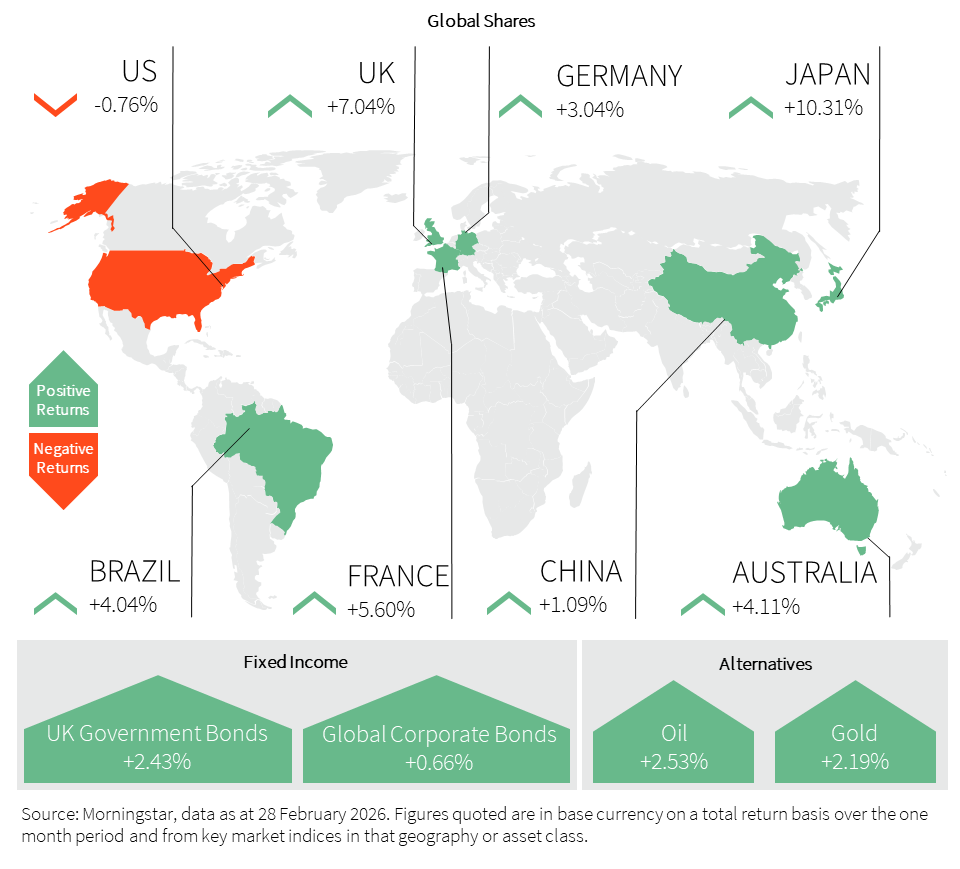

As US technology stock performance has stagnated, Asian tech has picked up the slack. This is most starkly shown by Korea’s KOSPI index already up close to 50%, helped by the likes of Samsung benefiting from soaring memory prices. Meanwhile, the ‘Magnificent 7’ are now trading at their cheapest valuation in ten years, as they have continued to deliver solid earnings, but share price performance has waned. As well as the sell-off in software stocks, the mounting capital expenditure from the ‘hyperscalers’ is leading to an increasing amount of unease amongst investors. Google’s century sterling-bond issuance raised some eyebrows, as the company hasn’t been around for much more than 25 years and this bond is the century issuance since Motorola’s issue in the run up to the dotcom bubble.

Tariffs added to the volatility, with the Supreme Court voting that Trump’s tariffs were unlawful, but the President quickly explored an alternative avenue whereby he has enacted a 15% universal tariff instead of the country-specific tariffs previously imposed. This proved beneficial to Japan and many emerging market countries, where tariff rates were previously higher.

With a large amount of this uncertainty rooted in the US, investors continued to seek refuge elsewhere, and most regions outperformed the US in February. Japan was particularly strong as the snap election resulted in a ‘super majority’ for Prime Minister Takaichi and further raised the prospect of fiscal stimulus.

Turning to the mixed economic data, where US Gross Domestic Product (GDP) growth was substantially weaker than anticipated, due in part to the government shutdown and easing consumer spending. Meanwhile, there were green shoots in manufacturing data, with the strongest private sector activity since 2022, providing hopes of a long awaited industrial recovery.

Our in-depth views on:

Our weightings are based on sterling as a base currency.

United Kingdom (UK)

The stars continue to align for UK equity markets as ‘old industry’ sectors become vital for the new AI world, whilst the defensive qualities and lower valuations offer a perfect foil when concerns over US valuations mount. The ‘Halo Trade’ is in full swing with ‘heavy assets, low obsolescence’ sectors like utilities, materials, industrials and energy driving the FTSE 100 to end the month at all-time highs. It has also been a month where earnings have taken centre stage with some of the largest components of the index like AstraZeneca, HSBC and Rolls-Royce reporting strong results, helping to lift the market.

There was good news for Rachel Reeves as a surge in capital gains tax, employers’ National Insurance contributions and a boost in income tax receipts created a larger than expected surplus in January to the tune of £30.4bn. This was the highest level since records began in 1993. There was also positive news on the inflation front with falls in petrol prices, air fares and food pushing inflation down to 3% in January, aligning with the consensus forecast. Gilt yields fell further through the month, providing hope that further tax rises will not be needed this year and generate an expectation that there will be few new announcements at the spring statement.

Prior to the events in Iran, expectations were for a further interest rate cut in March. Whilst holding rates in February, the Monetary Policy Committee (MPC) were split on a knife-edge, voting just 5-4 in favour of holding. With inflation normalising and the jobs market turning negative, committee member Alan Taylor predicted a further three interest rate cuts this year. For the three months to December 2025, the unemployment rate climbed to 5.2%, the highest level in nearly five years.

Flash Purchasing Manager Indices (PMIs) released for February continued to show an improvement for British businesses following the uncertainty created by last year’s budget. The composite PMI hit the highest level since April 2024. Retail sales data was also upbeat, with the fastest annual sales volume growth in around four years. House prices remain resilient, edging up again in February as the market picks up some momentum due to the lower mortgage rates available.

United States (US)

US equity markets underperformed in February as concerns over AI CapEx, returns on this spending, and the threat of AI to software providers continued to hit the dominant index positions of the ‘Magnificent 7’ stocks. As a group, they fell 7.3% through February. Encouragingly, rather than triggering a broader sell-off, we saw a broadening out and rotation into value and mid-caps with these areas outperforming. Old industry stocks in the DOW Jones drove it over 50,000 index points for the first time in history. Corporate earnings remained solid in Q4 2025 with year-on-year earnings growth of over 14%, the fifth consecutive quarter of double-digit earnings growth.

February saw tariffs back on the agenda and a major ruling on presidential power as the Supreme Court struck down the sweeping tariffs imposed by Donald Trump on Liberation Day. The court ruled 6-3 that he needed congressional approval to implement these. Branding the six judges as ‘a disgrace to our Nation’, Trump used section 122 of the Trade Act of 1974 to impose a global tariff of 15%, which can remain in place for 150 days. Consequently, more than 900 companies have now sued the US, raising pressure on the administration to issue refunds that could total over $160bn.

Growth for the fourth quarter of 2025 slowed more than expected from an annualised rate of 4.4% to 1.4%, missing forecasts of 2.5% growth. The federal government shutdown shaved over 1% off the figure, whilst personal spending on goods fell for the first time since the first quarter of 2024. Inflation data reported through the month was mixed, with Consumer Price Inflation (CPI) accelerating to 2.4%, which was slightly below the forecast. On the other hand, Producer Price Inflation (PPI) accelerated in January with goods outside the volatile food and energy category accelerating by the most in more than three and a half years. This reinforced the view that the Federal Reserve (Fed) may not cut interest rates again before June.

Europe

European equity markets navigated a turbulent February, characterised by a mid-month rally back toward record highs, followed by a sharp sell-off in the final days as geopolitical shocks erased much of the progress.

By the end of February, major bourses showed a marked contrast in performance. France (CAC 40) was the standout performer for most of the month, rising 5.6% as domestic fiscal clarity and strong earnings from luxury and industrial giants provided a lift. Germany (DAX 40) continued its momentum with a 3% gain, supported by the ongoing effects of Germany’s massive multi-year fiscal investment package. Italy (FTSE MIB) remained resilient for much of the month but was hit hard in the final sessions by a banking sector sell-off, closing significantly off its February peaks.

The European Central Bank (ECB) maintained a steady hand at its February 5 meeting, keeping the deposit rate at 2%. While January inflation had dipped to 1.7%, data released at the end of February showed a rebound to 1.9%, driven by rising services costs at 3.4%.

Economic sentiment was further rattled in the final weekend of the month by the escalation of conflict in the Middle East. Threats to energy infrastructure caused European natural gas prices to double, sparking immediate fears of a fresh inflationary shock and a ‘hawkish’ pivot from the ECB in the coming months.

Fixed Income

It was a strong month for government bonds, with prices rising and yields falling across major markets. Ten-year yields declined by around 0.2 percentage points in the US, UK and Germany, with the UK gilt ending the month at 4.23% and the US 10-year briefly dipping below 4%.

US Treasuries were supported by a broader risk-off environment triggered by the tech sell-off, renewed tariff concerns and escalating tensions in the Middle East. The yield curve flattened as the 10-year yield fell more than the 2-year, reflecting safe-haven demand at the long end. Meanwhile, the front end remained anchored by a cautious Fed stance after inflation surprised slightly to the upside, with headline Personal Consumption Expenditure (PCE) reaching its highest level since March 2024. Federal Reserve Open Market Committee (FOMC) minutes reinforced the view that policymakers prefer to delay interest rate cuts until clearer evidence of sustained disinflation emerges. Overall, macro data still broadly point to a ‘Goldilocks’ backdrop of moderating inflation and resilient growth.

In the UK, yields also moved lower, with the two-year falling slightly more than the ten-year as markets increased expectations for interest rate cuts. This followed softer inflation data, with CPI easing to its lowest level in almost a year, largely driven by lower fuel prices. While the Bank of England kept Bank Rate unchanged at 3.75%, four of the nine MPC members unexpectedly voted for an immediate cut, signalling growing confidence that inflation pressures are easing. However, escalating tensions in the Middle East could lead to renewed inflation risks via higher energy prices.

Japanese government bonds also rallied, with the 10-year yield declining by more than 0.1 percentage points. Yields initially rose following Takaichi’s election victory amid expectations of fiscal stimulus, but subsequently fell back after the government signalled it would explore funding sources for potential tax reductions without issuing additional debt.

Asia & Emerging Markets

Emerging markets held up well, delivering a 2.5% return in local currency. China lagged, with onshore markets rising around 1%. Asia ex-Japan led gains, supported by Korea and Taiwan, clear beneficiaries of the AI infrastructure build-out as US ‘hyperscaler’ capex feeds through to Asian semiconductor and hardware supply chains.

Japan was the standout performer, with the Nikkei rising around 10% in local currency. Markets reacted positively to Takaichi’s landslide victory, which gives her a strong mandate to pursue fiscal expansion, investment and targeted tax cuts, while also paving the way for higher defence spending in the coming years. On the macro side, inflation remains sticky in core components such as services and food, keeping overall price pressures elevated despite modest moderation in headline readings.

In China, policymakers continued targeted easing. Shanghai relaxed home-buying rules as part of broader efforts to support the property market, where indicators showed tentative improvement as the pace of second-hand price declines slowed. Meanwhile, the People’s Bank of China (PBoC) cut the foreign exchange forward risk reserve requirement to zero from 20%, to ease upward pressure on the renminbi. Risk sentiment improved toward month-end as liquidity returned following the Chinese New Year break and ahead of the upcoming ‘Two Sessions’.

Elsewhere, India reported strong credit growth and better-than-expected GDP, pointing to strengthening economic momentum, while the Reserve Bank of India (RBI) held interest rates unchanged despite low inflation, signalling a more hawkish stance. In Latin America, Brazil’s PPI remains in deflationary territory, supporting expectations for a 0.5% interest rate cut in March. Mexico’s GDP remained resilient on stronger services and industrial activity, while the central bank held rates at 7.0% but maintained a dovish bias.

Alternatives

February was a month of two distinct halves for global commodity markets. After a period of relative stability, the final days of the month were rocked by significant geopolitical escalation in the Middle East, leading to a ‘melt-up’ in energy and safe-haven metals.

For much of February, energy prices were suppressed by milder weather across Europe and high wind generation. However, everything changed on February 28 following a joint military operation by the US and Israel against Iran.

Brent Crude spiked to above $70 per barrel for the first time since July. Threats of a closure of the Strait of Hormuz, which carries 20% of global oil, introduced a severe risk premium.

The metals complex saw a sharp divergence between precious metals and industrial base metals. Gold hit record highs, briefly touching $5,500 per troy ounce in early February before consolidating near $5,200. Demand was driven by ‘safe-haven’ buying and central bank diversification. Silver showed even higher volatility, returning to levels last seen in the early 1980s as investors hedged against currency debasement.

Copper reached record peaks of $14,527 per tonne in late January/early February but spent much of the month consolidating. While long-term demand from AI data centres and green energy remains a ‘driver’, high exchange inventories (an 11-month high) acted as a detractor, capping further gains.

Tin was the standout performer as it surged toward $54,000 per tonne following a 47% month-on-month drop in Indonesian exports, highlighting the market’s extreme sensitivity to supply shocks.

Property

The UK property market in February was characterised by a ‘seasonal reawakening’, with a significant surge in new listings meeting a cautious but steady buyer base. While transaction volumes showed signs of recovery, price growth remained modest as the market adjusted to a “new normal” of stabilised interest rates.

February saw the highest number of new homes listed for sale in a decade, up 6% year-on-year. This influx of supply kept price growth in check; average asking prices remained virtually flat month-on-month at £368,019, though annual growth steadied at approximately 1.3%. Nationwide reported a slightly more optimistic 0.3% monthly rise, suggesting a ‘modest recovery’ following 2025’s year-end lull.

Borrowing conditions continued to improve, with average two-year fixed rates falling to 4.28%, their lowest level in four years. However, Bank of England data for the start of the year showed net mortgage approvals dipping to 60,000, a two-year low. This lag reflects the transition period as buyers wait for these lower rates to fully filter through into affordability before committing to purchases.

The rental sector saw a rare marginal cooling, with average UK rents dipping 0.1% in February to £1,301. This was largely driven by London, where rents fell for the fourth consecutive month to £2,067. Conversely, the North East and Scotland continued to see annual growth above 4%. Tenants are increasingly hitting affordability ceilings, leading to longer letting periods.

The commercial sector displayed a sharp divergence between asset classes. Offices remained the most in-demand asset, particularly in the West Midlands and the South East. In Central London, vacancy rates for prime offices hit a record low of 0.3%. Retail remained polarised; prime locations saw steady interest, but secondary high streets continued to struggle with higher vacancy risks. Within Industrial, demand for warehouse space remained robust, though growth slowed compared to the post-pandemic peak.

Learn more…

Important Information

All Index data figures are sourced by Morningstar and correct as at 28 February 2026, unless otherwise stated.

The value of investments or any income arising from them may fluctuate and are not guaranteed. Past performance is not necessarily a guide to future performance.