World Market Summary

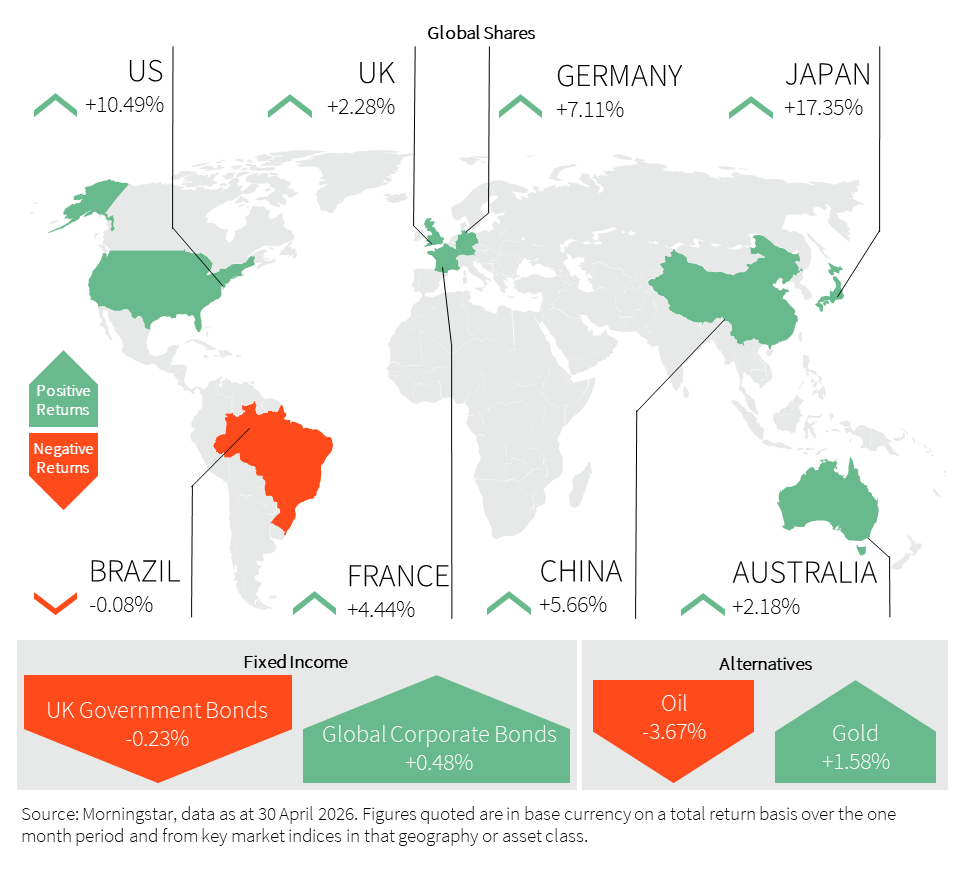

April was another month dominated by two forms of crude. Trump’s social media posts and the resulting oil price volatility. Yet, April has been a stellar month for equities with US stocks registering their best month since 2020. US tech earnings and Anthropic’s Mythos AI model provided the key catalysts for investors to set aside the geopolitical disruption and elevated oil prices. The Philadelphia Semiconductor Index saw a record 18-day winning streak as positive sentiment towards future tech earnings returned, and a heightened scarcity of memory chips builds. Consequently, the US and tech-focused Asian markets were the strongest performers over the month. Korea and Taiwan indices overtook the UK, leaving our domestic market as the 9th largest globally. This is quite the feat when you consider Korea’s market was half that of the UK at the beginning of 2024.

With the Trump and Xi meeting in May, the hope is for a resolution to the Middle East conflict. However, this is by no means a certainty, with both the US and Iran expecting the other to blink first. In the meantime, inflationary pressures and growth pressures mount amidst the elevated oil prices. Central bank meetings unsurprisingly struck a much more hawkish tone than before the war started, with the majority in ‘wait and see’ mode. Federal Reserve (Fed) Chair Powell also held interest rates steady in his final meeting after eight years as chair. Trump’s appointment, Kevin Warsh, will be the new chair, but will struggle to rationalise cutting interest rates in the current environment, as expectations are that the US Gross Domestic Product (GDP) growth has so far held up reasonably well. However, consumer confidence is at record lows, and if oil prices remain elevated, this will likely start to translate into hard data.

Our in-depth views on:

Our weightings are based on sterling as a base currency.

United Kingdom (UK)

The UK stock market endured a challenging and volatile April, as the geopolitical fever that gripped markets in late March continued to weigh on investor sentiment. After a promising start to the month, driven in part by a recovery in banking stocks, the index plateaued and subsequently gave back most of the gains it had accrued following an escalation in shipping disruptions in the Middle East.

However, the FTSE 250 showed some resilience after a torrid March, thanks mostly to more localised mergers and acquisitions (M&A) from private equity and international rivals as the valuation gaps between UK mid-caps and their US and European peers remained wide enough to finally prompt interest.

The Bank of England (BoE) dominated headlines in the middle of the month. Despite calls for a rate cut to stimulate a slowing economy, the Monetary Policy Committee voted 6–3 to hold the Bank Rate at 3.75%, citing ‘second-round effects’ on inflationary pressure from the March oil spike, which pushed inflation back up to 3.4%.

Conversely, the Office for National Statistics (ONS) reported a record tax haul for the start of the new fiscal year, providing the Treasury with unexpected headroom that fuelled rumours of an early summer stimulus package.

The Aerospace & Defence sector continued its run of strong performance as European governments accelerated procurement timelines. However, the Retail sector remained under intense pressure, with data showing a -49% contraction in sales expectations. Next and JD Sports saw significant selloffs following profit warnings linked to rising logistics costs, and thanks to the BoE’s hawkish decision to hold rates steady, housebuilders came under pressure as hopes for mortgage rate relief cooled, and the likes of Persimmon and Barratt Redrow, in the FTSE 100 saw heavy selling.

United States (US)

Investors looked past a complex, changeable, and fragile macro backdrop as US markets roared back in April to hit all-time highs through the month. Undeterred by a sustained elevated oil price and lack of progress in unlocking the Strait of Hormuz, the Nasdaq 100 led the charge, gaining 15.3%, its best monthly performance in 23 years, with the S&P 500 rising 10.5%. Although participation in the rally was broad, it was the return of the AI trade that stoked the fires, with Nvidia again surpassing the $5 trillion market cap and Alphabet following hot on its heels.

This US rally has been backed up by earnings. With around two-thirds of companies having now reported, 84% have beaten expectations, with earnings growth at the strongest level since Q4 2021. On average, companies are reporting earnings over 20% above average expectations, which is well above the five-year average of just over 7%. Of particular note has been indications of AI demand translating into returns, with Cloud revenue growth at Google up 63% in the quarter and Azure at Microsoft growing at 40%.

The month saw a number of economic indicators released. US GDP accelerated to an annual rate of 2% in the first three months of 2026, boosted by a rebound in government spending and a surge in business investment. AI infrastructure and data centre investment swelled 22%, displaying how the tech sector continues to drive the US economy. US retail sales grew strongly in March, albeit flattered by gasoline station receipts.

In what was Jerome Powell’s final meeting as Fed Chair, interest rates were held steady amidst a mixed but stable labour market, solid economic activity, but rising inflationary pressures. These pressures were confirmed later in the March data when the Fed’s preferred inflation gauge rose to 3.5% marking its highest rate in nearly three years.

Europe

The MSCI Europe index rose 6% in local currency terms, helped by Germany up 7.1% and supported by improving corporate earnings momentum. However, the macro backdrop remains fragile and geopolitically driven. The Eurozone is increasingly exposed due to its structural reliance on external demand and imported energy inputs, leaving it vulnerable to both demand slowdowns and supply-side energy shocks. Geopolitical risk continues to dominate sentiment. Stalled US-Iran negotiations, closure risks around the Strait of Hormuz, and elevated oil prices have kept risk appetite subdued. Eurozone economic sentiment has fallen to its lowest level since 2020, with consumer confidence weakening sharply for a second consecutive month. Industrial and construction sentiment has held up relatively better, but this divergence is unlikely to persist if energy prices remain elevated. Without a near-term geopolitical de-escalation, further deterioration in consumption is likely as higher energy costs and commodity constraints weigh on real incomes and production.

Inflation ticked higher in April, driven by energy, broadly in line with expectations. GDP growth slightly undershot consensus, partially due to a downside surprise in Ireland. Inflationary pressure is expected to intensify as the commodity shock from the Iran conflict feeds through more broadly. Consensus 2026 Eurozone growth forecasts have already been cut from 1.2% pre-conflict to 0.9%, with further downside risk if energy disruption persists.

Policy continues to remain in focus. The European Central Bank (ECB) held interest rates at 2% unanimously, but markets are now pricing an 89% probability of a 25bps hike in June, with up to three hikes expected by year-end. The tone of the press conference reinforced a high likelihood of a June move. However, further tightening risks exacerbating downside growth pressures while doing little to address supply-side inflation stemming from energy constraints.

Asia and Emerging Markets (EM)

Emerging markets had a very strong month, with the FTSE EM Index up 10.3%, led by Asia ex-Japan up 16%. The key driver was the semiconductor-heavy Korea and Taiwan complex, where stocks surged sharply as AI frontier models continued to exceed expectations, reinforcing demand visibility for advanced compute and memory. This has meaningfully shifted market perception around prior concerns of AI-driven capital expenditure overspend and earnings sustainability.

Japan was a standout performer, with the Nikkei up 17.3%. Gains were supported by policy cushioning, as government fuel subsidies and energy price caps helped absorb the inflationary impact of higher global energy prices, with inflation broadly in line with expectations. Against this backdrop, the Bank of Japan held interest rates steady but signalled further tightening to come, while markets continue to price two further hikes by year-end. The yen also strengthened over the period, widely attributed to suspected official intervention after breaching the critical ¥160 per dollar level.

China underperformed the broader EM index but still rose 5.7%. Activity data presented a mixed picture. While Q1 GDP surprised to the upside and both industrial production and exports held up better than expected, this was offset by persistent domestic weakness. The property sector remains the key drag, with investment and residential sales down double digits year-on-year, continuing to weigh on confidence and feeding through into weak retail sales. As a result, household demand remains the binding constraint. Growth is instead being supported by external demand and inventory restocking, which has driven import strength and cushioned the first-round impact of the energy shock.

Elsewhere, Brazil declined slightly in April as the Middle East shock fed through into higher fertiliser import costs, lifting this year’s inflation expectations and pushing up the interest rate outlook. This has reduced the expected cumulative easing to 0.2%, from 0.25% previously. India’s index, by contrast, remained resilient, rising 5.2% despite higher oil pass-through via Hormuz-related disruptions and some export weakness from elevated shipping costs and rerouting pressures.

Fixed Income

Bond market volatility eased but failed to return back to the level seen prior to the Middle East conflict. Bond yields also failed to ease to pre-war levels and on the whole actually continued to move higher in April. This was especially true at the longer end of the yield curve, where the UK 10-year government bond yield and the US 30-year government bond yield surpassed 5%. These moves were reinforced by central banks holding rates unchanged and issuing hawkish commentary. There was the Federal Open Market Committee, indicative of the level of uncertainty surrounding the future of inflation, growth and therefore monetary policy.

Credit spreads remain relatively tight, supported by continued stellar corporate earnings.

The dollar weakened slightly as the ‘flight to safety’ unwound, and investors moved back into risk assets. This took some pressure off the yen, which had briefly surpassed ¥160 against the dollar.

Alternatives

Oil markets remain under pressure as the ongoing Iran conflict continues to disrupt global energy supplies. Brent crude rose to over $110 a barrel towards the end of the month, while US gasoline prices remain near their highest levels since the conflict began. Iran has indicated it may accept an interim deal to reopen the Strait of Hormuz if the US lifts its blockade of Iranian ports, though disagreements remain over control of shipping. The prolonged closure has caused fuel rationing in parts of Asia and Africa and increased fears of a global slowdown. In a major development, the United Arab Emirates announced it will leave Organization of the Petroleum Exporting Countries (OPEC) next month, raising uncertainty over the organisation’s future and global supply coordination. Shell plc’s CEO warned that ongoing disruptions and lost production could lead to energy shortages lasting into 2027.

Gold continues to struggle. A stronger dollar and now rising treasury yields have combined to push gold into what many would describe as bear market territory. The key issue remains the conflict in Iran. With no clear resolution in sight, oil prices have stayed elevated, and higher energy prices are feeding into global inflation expectations, which informs monetary policy and impacts the price of gold. Major central banks continue their ‘wait and see’ approach. Gold typically benefits from inflation and geopolitical uncertainty, both of which are present. However, higher interest rates and the strength in the dollar that is currently coming from this situation are acting as a counterweight.

Property

UK house prices rose 3.0% year-on-year in April, marking the fastest pace since last May, according to Nationwide. The latest result topped market expectations and March’s 2.2% gain, with Chief Economist Robert Gardner noting the housing market has regained momentum despite Middle East tensions and higher energy costs. ‘This is somewhat surprising given that indicators of consumer confidence have weakened noticeably,’ he said, adding that higher interest rates and a more uncertain backdrop remain headwinds.

The Halifax price index showed house prices rose by just under 1%, below the expected 1.5%, marking the softest annual growth in three months. The average home was £299,677. The head of mortgages at Halifax noted that the slowdown is a reflection of geopolitical uncertainty. Higher energy prices have fuelled higher inflation expectations, pushing mortgage rates up and weakening confidence that interest rates will be cut this year.

UK construction PMI showed a slight improvement in construction activity but brought the length of contraction in the sector to over a year. The survey indicated that operating margins remained under pressure in the period due to a sharp acceleration in input cost inflation. Companies noted that the outbreak of conflict in the Middle East increased the prices of energy and raw materials used in projects.

Learn more…

For more industry terms and definitions, visit our glossary here.

Important Information

All Index data figures are sourced by Morningstar and correct as at 30 April 2026, unless otherwise stated.

The value of investments or any income arising from them may fluctuate and are not guaranteed. Past performance is not necessarily a guide to future performance.