Macro

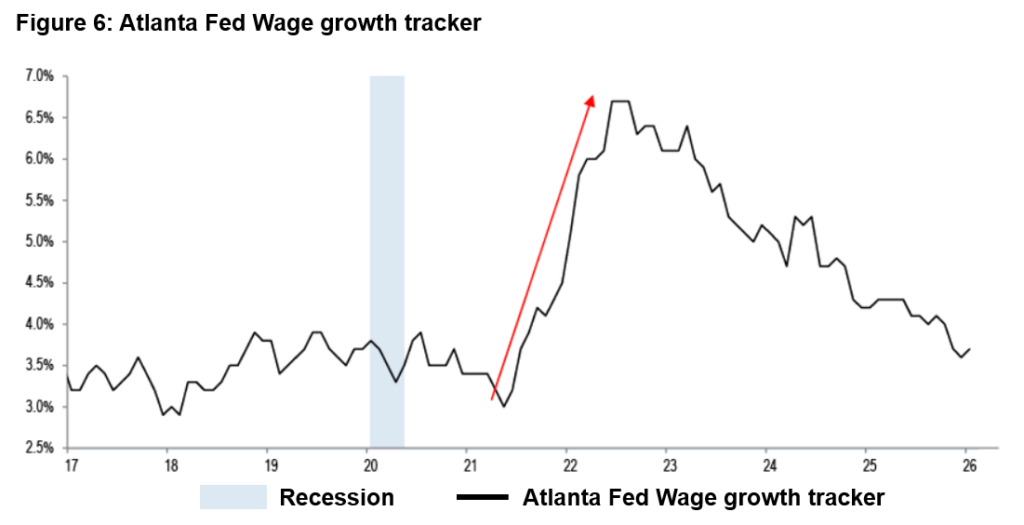

Economic data largely deteriorated in Q1 2026, and the strength that was witnessed could well fade as the elevated energy prices associated with the Iran war have an increasingly detrimental impact. Alongside the inflation concerns, global growth is also in jeopardy given the impact of higher energy prices on consumption, and this provokes a fear of stagflation. Ominously, the data was already feeding into this narrative before the war started, with US Producer Price Inflation (PPI) reaching its highest level since 2022 and US GDP dropping substantially from 4.4% to 0.7% in Q4. The Atlanta GDP Fed Nowcast is tracking GDP growth to recover to 2% for Q1, but this is still a marked decline from the Q3 figure of 4.4%.

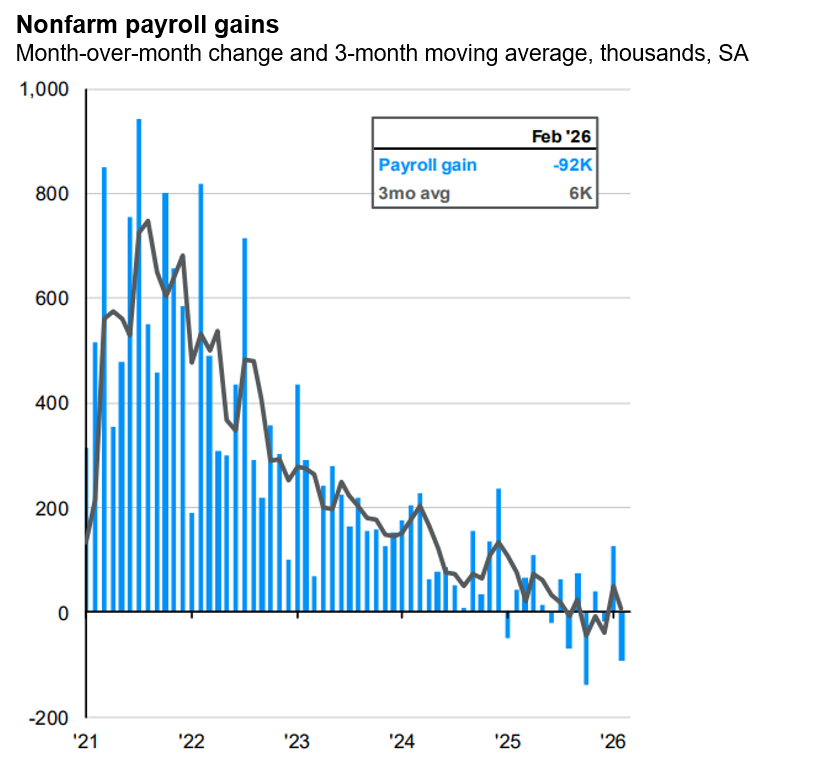

The labour market is also loosening dramatically, with private sector payrolls seeing their first decline in five years. The major winter storm has temporarily exaggerated this figure, but the downward trend displayed below remains clear.

More positively, manufacturing activity was seeing a revival heading into the war, with the February reading at the highest level since 2022.

Elsewhere, in response to the war, central banks largely took the same ‘wait and see’ approach as the Federal Reserve (Fed). Brazil provided an exception as it embarked on an interest rate cutting cycle from 2006 highs of 15%. UK and European consumer confidence dropped markedly as inflation started to pick up, with European consumer confidence at its lowest level since 2022.

The key determinant of the economic impact of the war will be its longevity. The ‘Liberation Day’ tariffs were quickly scaled back, and we have consequently seen five consecutive quarters of double-digit earnings growth from S&P 500 companies. However, in this scenario, the de-escalation is not simply reliant on the US President, and the economic impact is therefore likely to be more damaging.

Markets

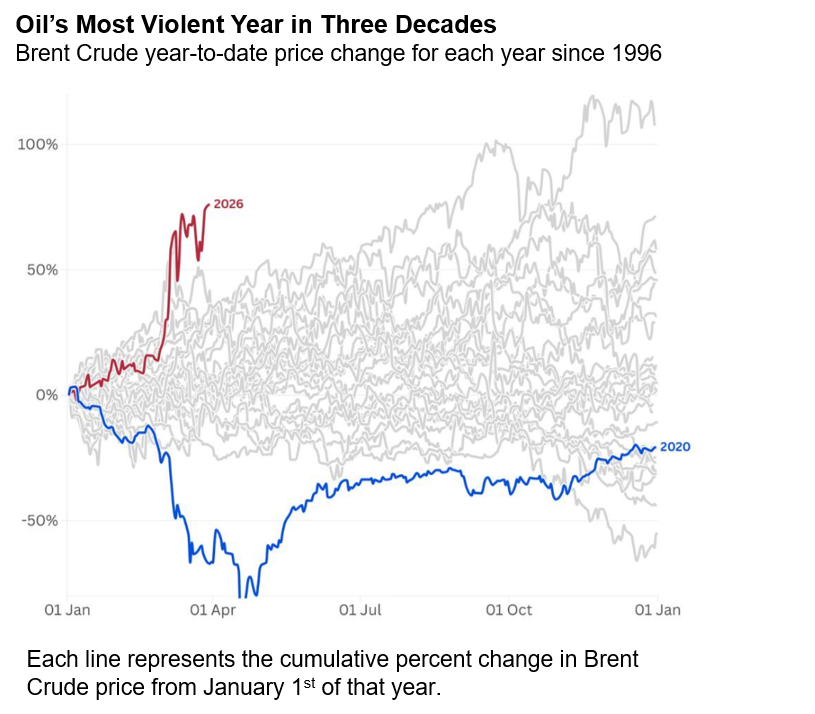

Q1 saw a rapid escalation in the geopolitical uncertainty that had already been a feature of markets since President Trump took office for the second time. However, equity markets continue to be impressively resolute in the face of this uncertainty, and oil prices are surging above $100 for the first time since 2022. This has particularly been the case for net energy exporters like the US and Brazil, which are better shielded from the oil shock. Very energy-dependent economies such as Korea and Japan have seen much more significant market sell-offs.

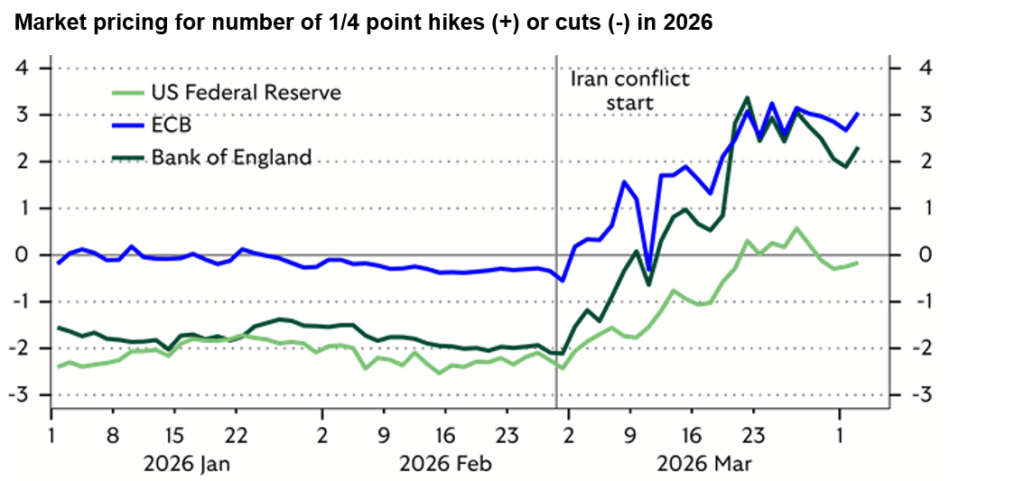

The quarter started with the US securing oil supplies by ousting Venezuela’s President Maduro, before later commencing a war in Iran. The four-year anniversary of the start of the war in Ukraine came and went, and we are now over four weeks into another war, with no obvious end in sight. The effective closure of the Strait of Hormuz will continue to keep oil prices elevated, given that 20% of global oil and natural gas trade passes through the narrow waterway. This puts upward pressure on inflation, and therefore bond yields have risen as expectations for interest rate cuts have evaporated, and markets are now pricing in a 40% of an interest rate hike in the US and are fully pricing three interest rate hikes in the UK and Europe. Whilst this move in bond yields has typically been at the front-end of the yield curve, Japan has seen its 10-year government bond yield reach its highest level since 1999.

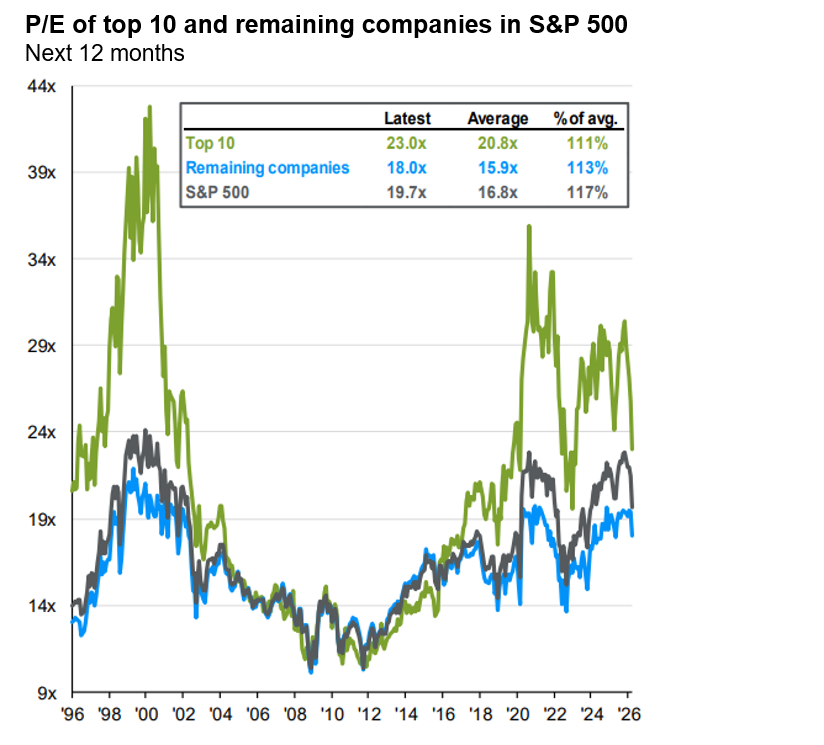

Prior to the start of the war, the release of Anthropic’s latest AI model caused a major sell-off in software stocks, amplifying the underperformance of US technology despite strong earnings from the world’s largest company, Nvidia, which expects its flagship AI processors to generate $1 trillion in sales through 2027. The ‘Magnificent 7’ are now trading at their cheapest valuation in ten years, as they have continued to deliver solid earnings, but share price performance has waned. As well as a sell-off in software stocks, the mounting capex from the ‘hyperscalers’ is leading to an increasing amount of unease amongst investors. Google’s century sterling bond issuance raised some eyebrows, as the company hasn’t been around for much over 25 years, and this bond is the century issuance since Motorola’s issue in the run-up to the dotcom bubble.

Positioning and Outlook

We highlighted in our previous commentary the importance of the low correlation that alternatives provide for a diversified portfolio. This was clearly demonstrated in this quarter as both bonds and equities sold off in the face of the war. Bond yields rose as investors feared an inflation shock, whilst equity investors focused on the potential for a growth shock and hit to earnings. Meanwhile, hedge funds and infrastructure, which sit in the alternatives bucket, have been able to generate a positive or very subtly negative performance since the war commenced. For infrastructure, the inflation-linked nature of the underlying assets makes it a safe haven in times of inflation fears. In the case of hedge funds, their ability to short equities and their use of stop losses* help to prevent excessive sell-offs and can result in positive performance even when equity markets fall.

*Stop loss: The automated exit from a position when losses hit a certain level or percentage

Turning to portfolio activity, where we have been able to make a number of changes to capitalise on a variety of opportunities where panic appears to have ensued. As long-term investors, we are able to look through these volatile periods and improve the quality of the portfolios whilst remaining highly disciplined on valuation. One such opportunity has been in US technology. The ‘Magnificent 7’ are now trading at their cheapest valuation in ten years, as they have continued to deliver solid earnings, but share price performance has waned.

Meanwhile, we also increased our exposure to a fund focused on the upgrade of grid infrastructure, which has sold off even though the war will likely only accelerate this upgrade cycle as countries and businesses look to reduce energy dependence and secure renewable power. To fund these opportunities, we have reduced our exposure to UK smaller companies, given the reduced growth prospects for the economy. However, we have increased our exposure to UK gilts given the seemingly excessive move in gilt yields, with the market now expecting more than three interest rate cuts.

Earlier in the quarter, we tweaked our Japan exposure to further capitalise on the ongoing corporate reforms and yen weakness, as well as tilting away from the weak domestic economy. In the sustainable models, we replaced an underperforming Asian fund with a very high conviction fund with similar exposure, and we increased the diversification of our infrastructure exposure.

We expect volatility to remain high for the rest of the year, and we will continue to be nimble to capitalise as and when opportunities present themselves.

Kind Regards,

Robert Matthews, Head of Research and Chartered Wealth Manager

Learn more…

Important Information:

For more industry terms and definitions, visit our glossary here.

All Index data figures are sourced by Morningstar and correct as at 31 March 2026, unless otherwise stated.

The value of investments or any income arising from them may fluctuate and are not guaranteed. Past performance is not necessarily a guide to future performance.