Summary

UK equity markets struggled to make headway in June. Despite a generally positive tailwind from corporate earnings expectations, particularly in the mining and energy sectors, there was a marked deterioration in market sentiment in the latter half of the month. This was largely driven by intensifying international ‘trade war’ rhetoric and a more hawkish US Federal Reserve stance on interest rates. This hawkishness was further reflected by the Bank of England’s June MPC amid still weak UK economic data, with parts of the UK retail sector clearly under great stress.

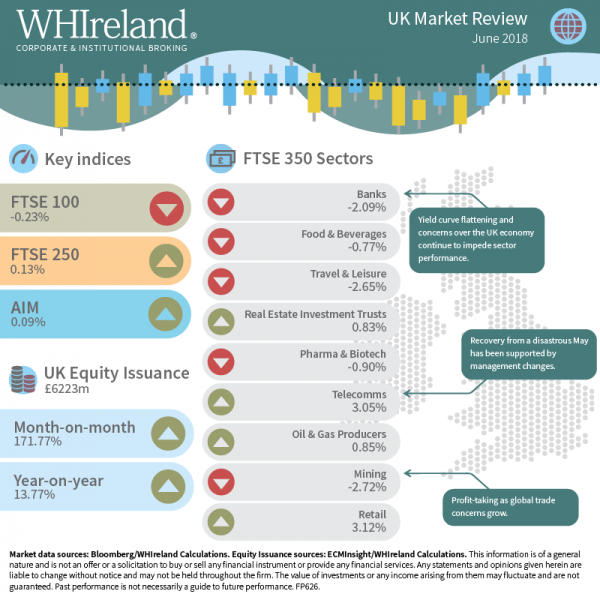

The Uk top 100, 250 mid-cap and AIM posted total returns of -0.23%, 0.13% and 0.09% respectively. Equity issuance increased markedly over the month, boosted by the UK government’s placement of part of its stake in RBS.

UK Equity Markets

Fairly flat UK markets in June did obscure some differential performance at the sectoral level, though not nearly to the same extent as seen in May. Much of the price action seemed to reflect a simple mean-reversion from recent out or under performance, though undoubtedly more fundamental factors were also in play.

Mining declined by 2.72% on the month as fears over a global trade war caused weakness in some industrial metals and prompted investors to take profits after a strong run in both April and May. The energy sector managed to close out the month with a 0.85% gain, capping a strong quarter, despite a late decision by ‘OPEC Plus’ to raise production in the belief that crude markets will otherwise overly tighten.

Having suffered a huge fall (-11.38%) in May, Telcos bounced by 3.05% in June to be one of the market’s better performers, aided by both management changes and the flattening of UK yield curves. Conversely, yield curve flattening – and the implied drag on profitability – probably contributed to another month of underperformance from the Banks, which fell 2.09% in June. Yield curve flattening and relatively supportive property price data over the month likely helped Real Estate Investment Trusts (REITs), post a modest 0.83% gain.

The Retail sector turned in another strong performance in June with a gain of 3.12%. Whilst this might seem counter-intuitive given some of lurid headlines the sector is currently generating in the UK press, it is worth drawing a distinction between food and non-food exposure. In the main, the former is managing to reprice in the face of higher inflation, while the latter is quite exposed to the resultant squeeze on UK household disposable income. Hence a relative performance of c. 30% in the first half of 2018 between the UK top 350 food and drug retailers and UK top 350 general retailers indices.

UK Economy

UK economic releases in June continued to disappoint, though not quite to the extent seen to May. PMI releases surprised on the upside, as did house prices, retail sales, net employment and public finances. Inflation indicators, including wage growth, performed largely in-line. However manufacturing and industrial production, construction, international trade and business and consumer confidence all fell short. The final reading of UK GDP for Q1 surprised some by being upwardly revised from 0.1% to 0.2%. However, analysis suggests that this was supported by stock building (which can be expected to subsequently unwind) and consumer spending supported by continued dis-saving (which will almost certainly rise).

Given this backdrop it was somewhat surprising that the Bank of England’s 21 June vote to keep interest rates on hold was closer than expected, with Chief Economist Andy Haldane joining the hawks to make it 6/3. To further muddy the waters, the accompanying statement and minutes sounded hawkish, while warning of increased risks around Brexit. At the time of writing, the overnight index swap (OIS) market suggests that there is roughly a two in three chance that the Bank of England will raise rates by a quarter of a point at its next meeting on 2 August.

UK Equity Issuance

June was a strong month for equity issuance at £6223m, representing a 171.77% increase on a lacklustre May and a 13.77% increase on June 2017. However this strong headline activity was dominated by the UK Government’s c. £2.5bn placement of RBS shares, which therefore accounted for just over 40% of the monthly total. Adjusting for this transaction, June’s total still amounted to a healthy £3717m, up 62.30% on the month. The number of announced deals also increased to 41 from 34 in May. Despite the greater level and breadth of activity, both investors and issuers are still evidencing heightened selectivity.

At the sectoral level, activity was somewhat more concentrated in June than in May, even allowing for the RBS placement distortion. Banks, financial services and general industrials each accounted for more than 10% of the total capital raised, while chemicals, equity investment vehicles; mining; oil & gas producers; real estate investment trusts and travel and leisure offerings all made meaningful contributions. Overall, the sector count fell to 17 from 19 in May.