Macro

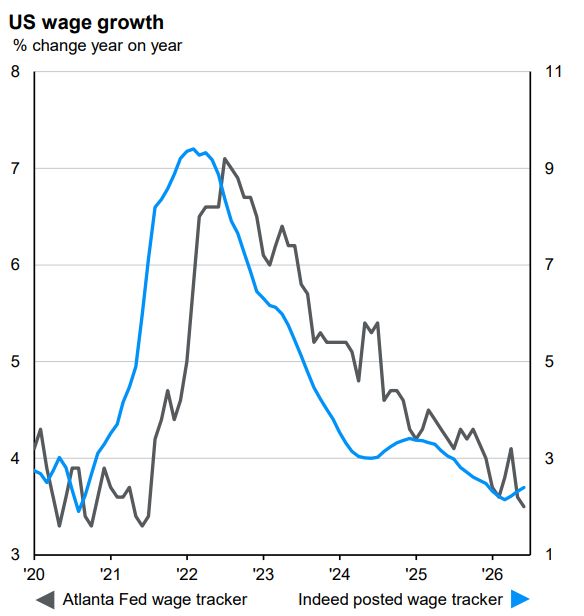

Economic data in the quarter provided a complicated backdrop for the Federal Reserve (Fed). US core Personal Consumption Expenditure (PCE) hit the highest level since 2023 at 3.4%, which is well in excess of the Fed’s 2% target. Consumer confidence picked up from record lows as oil prices fell. Economic growth and the labour market are also showing signs of stabilisation, but given the fall in oil prices and wage growth remaining in a disinflationary trend, the Fed will likely keep interest rates on hold over the coming months.

Fed chair Kevin Warsh has also highlighted the potential for AI productivity to put downward pressure on inflation, and given that he was appointed by Trump with the hope of lowering interest rates, we still anticipate a more dovish tilt from the Fed than the market is currently expecting, with more of the same from June’s decision to maintain interest rates at the current level.

In the UK, GDP growth improved and retail sales data came in, easing ahead of consensus expectations. Meanwhile, inflation remains more contained than in the US. Core inflation came in below expectations at 2.6%, close to a five-year low. Alongside the Fed, the Bank of England decided to keep rates constant, but given where inflation is, the central bank has a greater capacity to cut interest rates in the coming months. The European Central Bank ended its interest rate-cutting cycle, opting for a hike in response to the pick-up in inflation.

In Asia, China’s economic data remains very weak domestically, with the first contraction in retail sales since the pandemic. Fixed asset investment also contracted more heavily than expected. Exports remain the bright spot, surging 19.4% to hit another record high. Unlike in China, Japan’s domestic economy is strengthening with GDP growth improving from 0.7% to 1.8% in Q1. Inflation also remains well embedded in the economy, with wage growth expanding for the 52nd consecutive month and at the fastest pace since December 2024. The Bank of Japan consequently hiked interest rates, but this only exacerbated the weakness in the yen, which surpassed ¥160 against the dollar.

In contrast to the broader trend, Brazil continued with interest rate cuts as oil prices subsided.

Markets

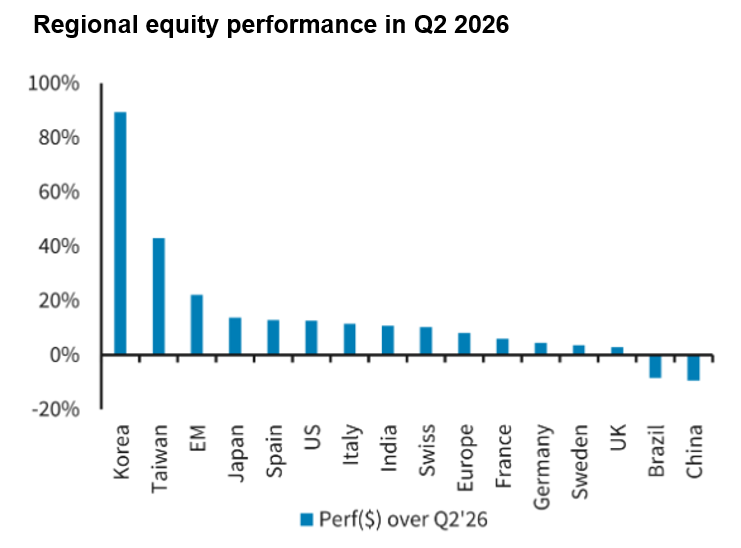

Stock prices continued to rise for much of the second quarter of 2026 despite the surge in oil prices associated with the Middle East conflict. The S&P 500 registered nine consecutive weeks of gains for the first time since 2023. Earnings strength, particularly for companies linked to the vast amount of Artificial Intelligence (AI) capital expenditure (CapEx), was the primary driving force of the rally. Memory chip prices surged, generating stellar earnings for Micron, helping tech-heavy South Korea and Taiwan markets to overtake the UK in terms of market capitalisation.

Surprisingly, as tensions in the Middle East subsided and the oil price moved lower, stocks fell back due to the hawkish comments from Fed Chair Warsh. Market weakness towards the end of the quarter was amplified by customers of memory chip-makers such as Apple and Microsoft attempting to pass on the higher costs, announcing price hikes in June. The record Initial Public Offering (IPO) from SpaceX, which pushed Musk to dollar trillionaire status, initially gained significant of traction with investors before the stock fell back along with broader US tech sentiment. Thus far, the old adage of ‘sell in May and go away’ has proved a good strategy. Still, earnings remain strong and grounded in fundamentals, which enables us to remain optimistic for equity performance prospects in the coming months.

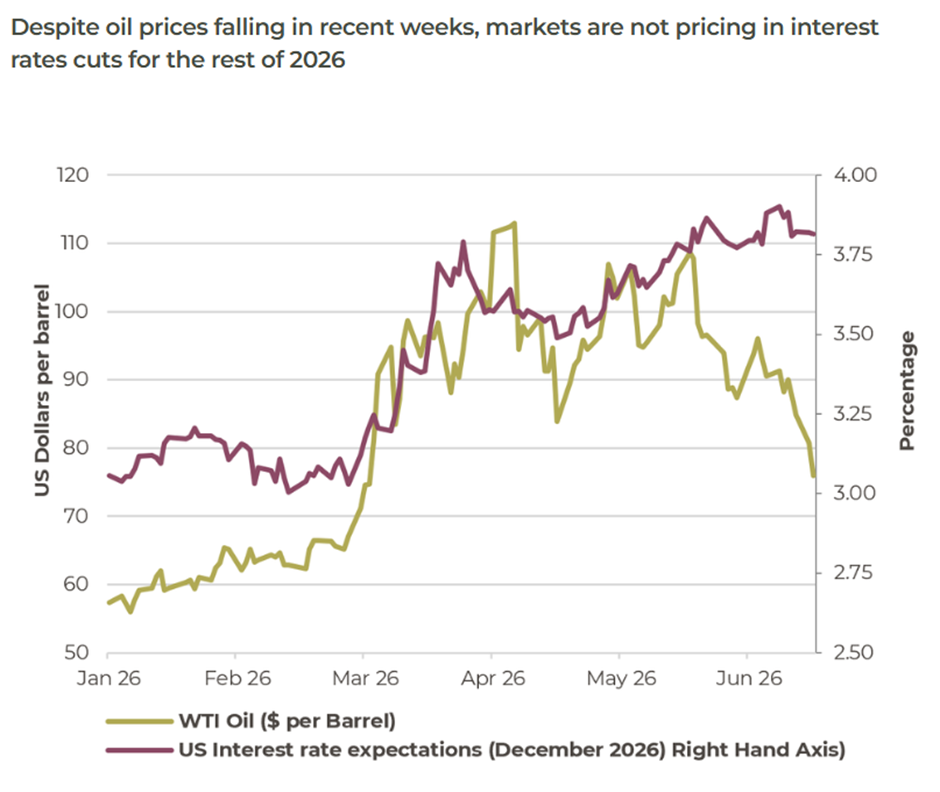

Brent crude oil saw a remarkable drop off towards the end of the quarter, now sitting close to $70 per barrel after spending most of Q2 2026 in excess of $100. This is very helpful for the global economy, and encouragingly, the price could move lower still, with many oil producers ramping up supply during the Middle East conflict, and the recovery of the major oil and gas terminal, Ras Laffan, looks to be well ahead of initial fears. Aside from ‘black gold’, the yellow metal’s performance was also challenged, dropping below $4,000 for the first time since November 2025 after a very strong run. The key catalyst was the hawkish commentary from Warsh, which led to a strengthening in the dollar and provided reassurance of the Fed’s independence. Treasuries were largely unmoved, as displayed in the chart below, due to Warsh’s commentary, but gilts rallied and were able to largely look through the resignation of the UK’s Prime Minister, Kier Starmer and rallied in response to the oil move.

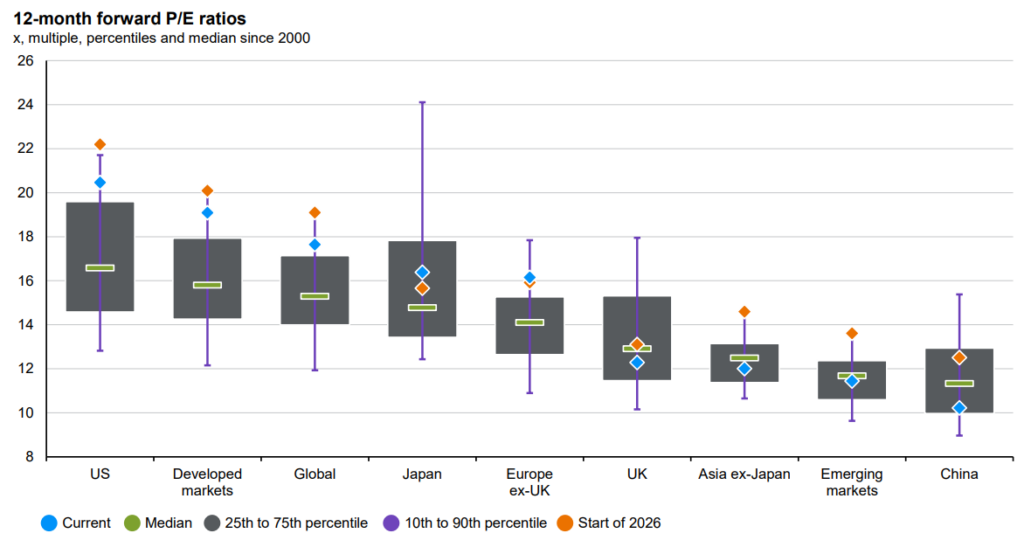

Earnings have continued to be very strong, with S&P 500 earnings growing at an impressive 19% run rate. Price movements have therefore not been devoid of earnings and have largely moved in lockstep. If anything, prices have struggled to keep pace with earnings in bottlenecks like that within memory chips. Hence, US valuations are not cheap but sit below the level they entered 2026.

Towards the end of the quarter, there was a clear rotation away from these slightly elevated valuations, into more unloved growth sectors like healthcare and regions like India. We have meaningful exposure in all these areas, as well as the UK, which also offers key diversification in periods where the heat comes out of the AI trade.

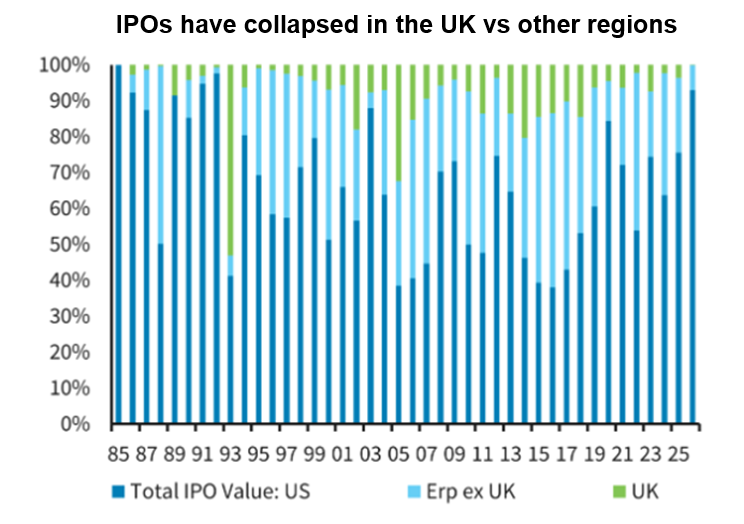

With earnings still growing very strongly and valuations reasonable, we are still positive on the outlook for US equities. However, with the midterms on the horizon and equity issuance ramping up from IPO’s such as SpaceX and Anthropic to come as well as equity raises from the likes of Alphabet, there could well be downside pressure and periods of volatility in the coming months. As well as the lack of AI exposure, the UK offers clear diversification here, with minimal issuance and elevated buybacks.

Turning to portfolio activity, where we added to AI exposure at the start of the quarter as valuations pulled back after the start of the Middle East conflict. We also added some UK property exposure to position ourselves for the Bank of England’s greater prospects of cutting interest rates.

We expect volatility to remain high for the rest of the year, and we will continue to be nimble to capitalise on opportunities as and when they present themselves.

Kind Regards,

Robert Matthews, Head of Research and Chartered Wealth Manager

Important Information:

For more industry terms and definitions, visit our glossary here.

All Index data figures are sourced by Morningstar and correct as at 30 June 2026, unless otherwise stated.

The value of investments or any income arising from them may fluctuate and are not guaranteed. Past performance is not necessarily a guide to future performance.