World Market Summary

Commodities had a bumper year in 2025, but have seemingly found another gear, taking no time to put the pedal to the metal in 2026. Global equities have also continued to drift higher as a number of the ‘Magnificent 7’ beat earnings estimates. Impressively, these returns have been generated in an environment of geopolitical tumult and a material sell-off in precious metals on the back of the announcement of the new chair of the Federal Reserve (Fed).

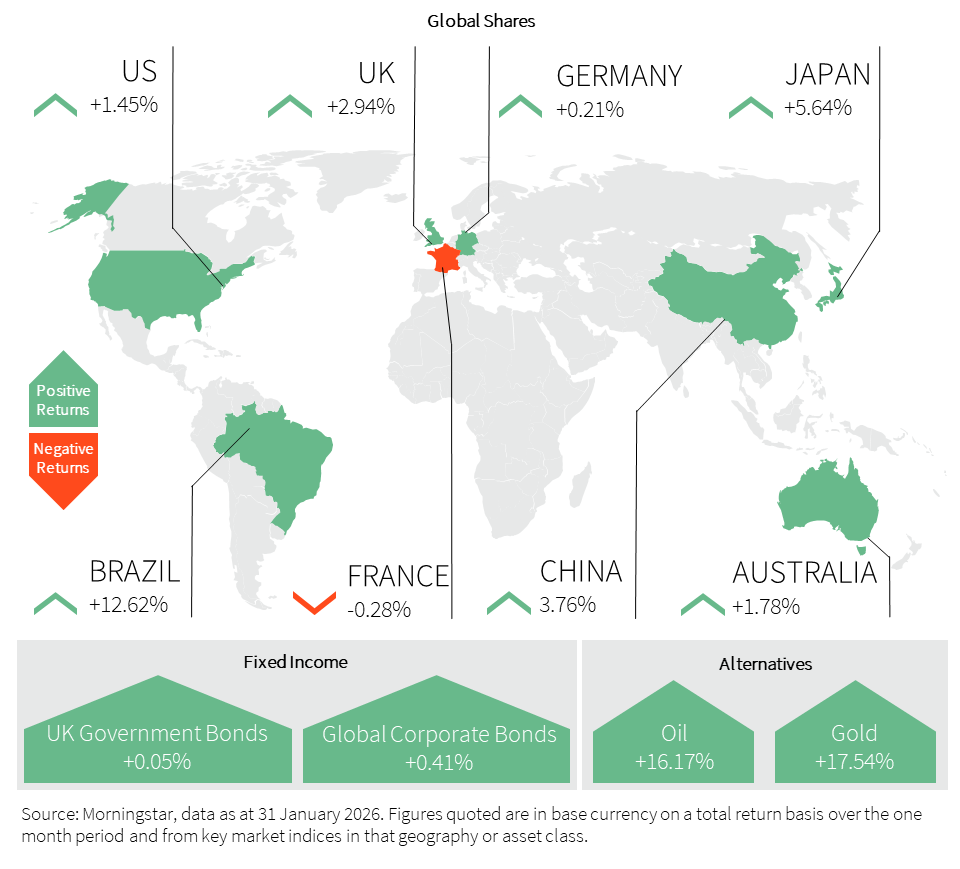

Tesla’s shift away from electric vehicles to robotics and Meta’s increased capex plans were greeted positively by the market, but Microsoft’s earnings beat was not sufficient to allay concerns over the growth miss for its cloud services segment, Azure. This segment grew at 39% and Microsoft’s shares sold-off 10%, demonstrating just how demanding Wall Street’s expectations have become for the ‘Magnificent 7’. Returns have consequently broadened to areas where positive earnings surprises are more attainable. This is demonstrated by US smaller companies outperforming larger companies, with the Russell 2000 returning 5.31% in January compared to the S&P 500’s 1.45%, but also larger companies outside of the US outperforming the S&P 500, with the FTSE 100 up 2.94%, MSCI Asia excluding Japan up 8.21%, and MSCI Europe excluding UK up 2.92%.

The World Economic Forum in Davos proved timely, immediately following the US’ capture of Venezuela’s president Maduro and the attempted acquisition of Greenland. Trump provided reassurance that the US would not turn to military force and having threatened tariffs on Europe, a ‘framework’ deal has subsequently dialled down tensions. Nevertheless, Canadian Prime Minister Mark Carney’s words from the forum appear to hold true, ‘The old world order is not coming back. We are not witnessing a transition to a new system. We are living through the end of the old one.’

Earnings, and subsequently markets, continue to be propped up by strong economic data and the prospect of further interest rate cuts. To the former, US Gross Domestic Product (GDP) continues to track well ahead of trend growth, with a figure of 4.4% in Q3 and the Atlanta Fed GDP nowcast sitting at 4.2% for Q4. For the latter, although not as dovish as the market’s expected candidate, the new Fed chair, Kevin Warsh, is a supporter of Trump and more likely to cut interest rates than current Chair Powell.

Markets are likely to remain volatile, with the ongoing jitters evidenced by Japan’s 10-year Government Bond yield hitting its highest level since 1999, gold shedding $2.5 trillion in a 30-minute period and yet oil and gold both registered double-digit gains for the month.

Our in-depth views on:

Our weightings are based on sterling as a base currency.

United Kingdom (UK)

UK markets enjoyed a fine start to the year, with UK indices being one of the best global performers in January. For the first time in its history, the FTSE 100 surpassed the 10,000-level, gaining just shy of 3% in the month. Strong earnings from the financials, positive performance from commodities, and momentum in defence stocks helped lift the index. In contrast to much of last year, there were signals of improving appetite for UK mid and small-caps, with the FTSE 250 gaining 3.68% as domestic business activity appears to be rebounding following Budget uncertainty. As relations with the US sour, Keir Starmer has looked east, meeting Chinese Premier Xi in the hope of fostering the UK footprint in China.

Never far from the headlines, President Trump threatened the UK and Europe with tariffs over Greenland before dropping the threat just days later. Aside from this, news coming out of the UK was fairly positive through the month. November’s GDP release beat forecasts, expanding 0.3% against a consensus of 0.1%. A significant portion of this growth was due to Jaguar car production returning following the disruption caused by a cyber-incident. Purchasing Managers Index (PMI) data showed the private sector entering 2026 with significant momentum post-Budget, which is encouraging. Manufacturing hit a 17-month high, supported by a rise in exports, and services registered sharp growth, boosted by technology and financial services.

Inflation data overshot expectations with a 3.4% rise for December, above the expected 3.3% rise. The figure was driven higher by air fares and an increase in tobacco duty. Whilst the Bank of England continues to forecast inflation at target in the second quarter of this year, of concern must be stubborn shop price inflation, which is at its highest in two years. Rachel Reeves’ Budget measurers appear to be passing on to the consumer, whilst demand for fresh foods is also driving up prices.

As Budget uncertainty passes and interest rates continue to fall, all eyes will be on whether the UK domestic housing market strengthens in 2026. Initial signs are encouraging, with house prices rising 0.3% in January. Nationwide is predicting prices to rise by between 2-4% this year, with house builders generally reporting an uptick in viewings as we enter the crucial spring selling season.

Business confidence continued to improve, albeit from low levels, extending the gains seen post-Budget, but it remains in deeply negative territory. Consumer confidence declined, with consumers across all 12 regions reporting a worsening in their financial well-being. This is, in most part, attributed to concerns over job security and slowing in wage growth. Nevertheless, this lack of confidence did not stop a strong December of retail sales with growth of 0.4%, far surpassing the 0.1% decline that was expected.

United States (US)

US equity markets started the year in a positive fashion with the S&P 500 up 1.45%, surpassing 7,000 index points for the first time. ‘As goes January, as goes the year,’ so the saying goes. Notching positive returns in the first month of the year has, on average, since 1945, led to the S&P 500 gaining 16.2% through the year. Hence, with the S&P 500 up 1.5% and the Nasdaq up 1.2%, it has been a good start, and importantly, there has been a healthy breadth of participation in this high-level figure.

That said, the month was not without volatility, with US markets underperforming many global peers as Trump’s actions once again created an uncertain backdrop both domestically and abroad. Firstly Venezuela, then onto Greenland and as we exited the month with a ‘huge US armada’ was moving towards Iran. Amidst this, the dollar has continued to weaken with gold flashing past $5000 an ounce before a violent reversal of this trade on the last day of the month. Despite beating earnings estimates, Microsoft shares shed 10%, wiping off over $360bn in value and reminding investors of the high expectations priced into AI darlings.

Trump renewed his attacks on the Federal Reserve, labelling current chair Jerome Powell a ‘moron’ who was ‘hurting our country and national security’. This was in response to the Fed’s decision to hold interest rates steady at its latest meeting. Fed officials cited a strong labour market, a strong economy and an uncertain inflation trajectory for their ‘wait-and-see’ approach. As we ended the period, Trump confirmed inflation ‘hawk’, Kevin Warsh as his nomination for the next Fed Chair which eased concerns over future Fed independence.

There was mixed news on the inflation stage, with encouraging core inflation data, which came in at its lowest level in several years at 2.6%. However, Producer Price Inflation (PPI) came in ahead of expectations, increasing at its fastest rate in five months, suggesting some pass-through from import tariffs, which may influence the timing of future interest rate cuts.

Despite tariff concerns, the US economy surged in Q3 2025 at its fastest pace in two years, at 4.3%, far surpassing the 3% expected. Consumer spending accelerated, exports climbed, as did government spending. There was less positive news on the consumer confidence front as sentiment dropped sharply in January, marking its lowest level since 2014. Pessimism over jobs, prices and economic prospects dampened consumers’ outlook.

Europe

The MSCI Europe had a solid month in January, rising 2.92%, reflecting broad investor optimism despite ongoing volatility. The German DAX gained 3%, supported by stronger-than-expected GDP growth and consumer confidence figures. In contrast, French CAC 40 fell 0.28%, weighed down by underperformance in luxury and consumer discretionary stocks amid concerns over slowing high-end consumption and soft Chinese demand. Cyclicals and energy showed relative resilience, while financials remained steady as markets priced in moderate rate-cut expectations. The euro traded in a narrow range, supported by stable Eurozone growth data but capped by weaker structural growth compared with the US.

Geopolitics remained a key overhang. The Greenland episode underscored renewed transatlantic tensions and highlighted Europe’s strategic vulnerabilities in the Arctic and critical minerals supply chains. While immediate tariff threats were eased, a modest geopolitical risk premium persisted in energy, defence, and infrastructure-linked sectors.

At the World Economic Forum in Davos, Europe’s lag in productivity and technology relative to the US and China was highlighted, emphasising the need for regulatory reform, integration, and industrial policy coordination.

On the macro side, the Eurozone economy grew 0.3% in Q4 2025, exceeding expectations and marking nine consecutive quarters of expansion. Spain led growth at 0.8%, with Germany and France posting 0.3% and 0.2%, respectively. Full-year 2025 GDP is estimated at around 1.5%, slightly above potential, while the ECB expects 1.2% growth in 2026 and is likely to hold rates at 2%.

Asia and Emerging Markets (EM)

January 2026 showcased a starkly divided performance across Asian and Emerging Markets (EM). While Japan and Hong Kong found reasons for optimism, India and mainland China grappled with structural headwinds and pre-Budget anxiety.

Japan’s Nikkei 225 returned 5.64%, fueled by the first manufacturing expansion since June 2025. A weakening Yen further buoyed heavyweight exporters, as the prospect of a snap election put downward pressure on the currency.

Hong Kong recorded its best monthly performance since September. Sentiment was bolstered by a one-year US trade truce and Beijing’s ambitious goal to triple semiconductor production by 2026. Beyond tech, ’premiumization’ was a clear theme; Macau casino stocks outperformed as gaming revenue grew 24% year-on-year. Vietnam was the EM standout, surging on a 9.2% rise in industrial production, a massive 48% jump in tech exports and the government’s push for MSCI to designate the country with EM status.

India faced a difficult month, with the Nifty 50 and Sensex falling over 3%. Investors grew cautious ahead of the Union Budget 2026, fearing changes to capital gains tax. This weighed on the Indian Rupee, which hit a record low of 92.02 per dollar in late January.

In Mainland China, the Shanghai Composite increased 3.76% to breach 4,100 index points, yet high trading volumes in AI and batteries couldn’t mask weak PMI data, which underlined persistent economic imbalances.

The capture of Nicolás Maduro in early January transformed the EM landscape. A subsequent 50-million-barrel oil deal with the US and the lifting of sanctions provided a ‘safety net’ for commodity-rich nations like Chile and Saudi Arabia, stabilising fiscal balances despite modest global growth.

Fixed Income

Despite the volatility elsewhere, the bond market remains remarkably sanguine, with volatility continuing to decline and now sitting near five-year lows. Credit spreads also remain at very tight levels, with corporate balance sheets remaining in good shape and the market seeing no reason for concern. The yield curve continued to steepen as the prospect of interest rate cuts remains on the table, but concerns over fiscal credibility urge investors to request greater compensation for taking on longer-term debt.

The Fed kept interest rates unchanged as growth surprised to the upside, and the labour market is providing no reason for major concern. However, when Kevin Warsh replaces the current Fed Chair, there are concerns that Trump’s influence on Warsh may result in interest rate cuts even if the economic data does not warrant them. Having previously worked on the Fed board, Warsh does possess more credibility than the bookies’ favourite, which has helped the dollar to recover, but the currency remains at five-month lows.

Meanwhile, the yen still remains very weak against the dollar. This weakness was supported by the announced snap election for February, in which the newly elected Prime Minister Takeichi will look to capitalise on her strong approval rating to enact further fiscal dominance. This, in turn, resulted in the 10-year government bond yield reaching its highest level since 1999.

Alternatives

Gold had a stellar month in January, just three days after breaking through $5,000, the price surged past $5,500 per ounce, reaching a high of $5,634. At the heart of the rally is a combination of uncertainty, policy risk and a weakening dollar, all culminating simultaneously. Investors continue to pile into safe-haven assets as geopolitical tensions rise and economic confidence in the US dollar frays. Trump’s comments suggesting he is content with the dollar’s weakness have unsettled markets, reigniting concerns around monetary debasement. Markets have also taken into consideration who will replace Chair Jerome Powell later this year, and expectations that interest rates could be cut under new leadership raise the prospect of a weaker dollar and higher inflation, which are conditions that historically been supportive of gold. While this move is unprecedented, the forces behind it are not random; a weaker dollar, political pressure on central banks, escalating geopolitical risk and a broader loss of confidence have combined to push investors toward assets that don’t rely on policy promises. On the news of Kevin Warsh’s appointment, gold shed $2.5 trillion in a 30-minute period but still registered double-digit gains for the month.

Brent Crude finished the month of January at approximately $71 per barrel, up more than 13% over the month. Rising unrest in Iran and the aggressive US rhetoric added to the geopolitical risk premium with fears that disruptions via the Strait of Hormuz would materially impact supply. Nonetheless, global supply continues to exceed demand, with non-Organization of the Petroleum Exporting Countries (OPEC+)producers such as Brazil and Canada pumping record amounts of oil. We may well see oil drop back down if and when these fears fade.

Property

In January, the Nationwide House Price Index rose 1% year on year, surpassing the expected 0.7% and picking up from the 0.6% gain in December. Housing activity likely dipped at the end of the year due to uncertainty over property tax changes, but mortgage approvals remained near pre-pandemic levels. Robert Gardiner, the Chief Nationwide Economist, mentioned that affordability improved over the past year, supported by earnings growth outpacing house prices and a steady decline in mortgage rates, which helped sustain buyer demand. First-time buyer activity also continued to rise, with many benefitting from relatively low mortgage payments.

The Royal Institution of Chartered Surveyors UK Residential Market Survey showed the house price balance held steady at -14% in December 2025, unchanged from November but slightly improved from the recent low of -19% in October. While this still points to a modest national decline in prices, the trend appears to be stabilising.

The S&P Global UK Construction PMI picked up in December from the over-five-year low in the previous month, but the reading still reflected a full year of monthly contractions for the second-sharpest decline since the Covid pandemic shock to the sector. Companies in the sector cite fragile confidence for clients that resulted in a sharp reduction in new orders to replace completed projects. Surveyees also noted that clients delayed investment decisions due to uncertainty of how the UK’s new Budget would alter their sales pipelines.

Learn more…

For more industry terms and definitions, visit our glossary here.

Important Information

All Index data figures are sourced by Morningstar and correct as at 31 January 2026, unless otherwise stated.

The value of investments or any income arising from them may fluctuate and are not guaranteed. Past performance is not necessarily a guide to future performance.