Many investors may have heard the term FANGS in passing or on the news, but what are they? FANGS are an abbreviation of Facebook, Amazon, Netflix and Google (Subsidiary of Alphabet); the acronym highlights some of the latest contributors to US technology which has seen an acceleration in equity returns.

Valuations in the industry are generally high as investors are focused on revenue growth and high operating margins, that hopefully in the future will translate into profits. Another key characteristic has been their ability to gain market share either by acquiring rivals or by superseding markets with superior technology to increase competition. This has driven market returns in recent history. The critical element to this is valuations must be justified by strong operational performance at some point. If the market loses confidence in a product or company, there is a long way to fall to get to comparable valuations of mere mortal businesses.

There are also several legislative threats to the industry as government agencies try to catch up with the innovations being made in the sector.

This can go to the extreme of banning operations. In the case of UBER, several European countries have banned the taxi hailing application, with a range of legislation from working practices, unfair competition methods and metering requirements.

There are also plans for governments to capitalise on significant profits made by tech companies in their own regions. Technology may face more tax under a new EU directive. Companies that generate online revenue could be subject to a 3% tax on revenue. It is expected to generate €5bn in new tax revenue. The largest technology firms pay an average of 9.5% compared to 23% for traditional businesses. This legislative backdrop is only likely to grow, with a new focus on online advertising to children and use of personal information data analytics to name a few.

Conclusion

FANG characterises an unfortunate combination of companies that ‘muddies the waters’ on the true representation of the Technology sector. The wide sector is a mix of real businesses generating meaningful profits at slower levels of growth, like Google’s Alphabet. In stark contrast, some constituents are high growth companies, some of which will change the face of how we work and live while others have flawed business models that are unlikely to materialise into profitable businesses in their current form.

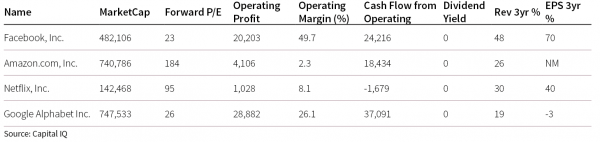

One thing to note is none of the FANGs pay a dividend; the focus is on capital growth. Therefore the higher the valuation investors are willing to pay, the more reliant returns will be on future growth expectations. The sector has a higher level of risk as investor sentiment is high, with share returns not necessarily corresponding to operational excellence. We feel for most private clients, a specialist fund manager would be the best way to invest in the sector and a longer term investment horizon is required.